How to Refinance Your Mortgage in Canada: Save Thousands in 2026

Struggling with high mortgage payments in 2026? Refinancing could slash your interest costs and save you thousands, especially as around 60% of Canadian borrowers face renewals this year with potentia...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Struggling with high mortgage payments in 2026? Refinancing could slash your interest costs and save you thousands, especially as around 60% of Canadian borrowers face renewals this year with potential payment hikes of up to 20%. Whether you're eyeing lower rates, accessing home equity, or consolidating debt, this guide walks you through how to refinance your mortgage in Canada step by step.

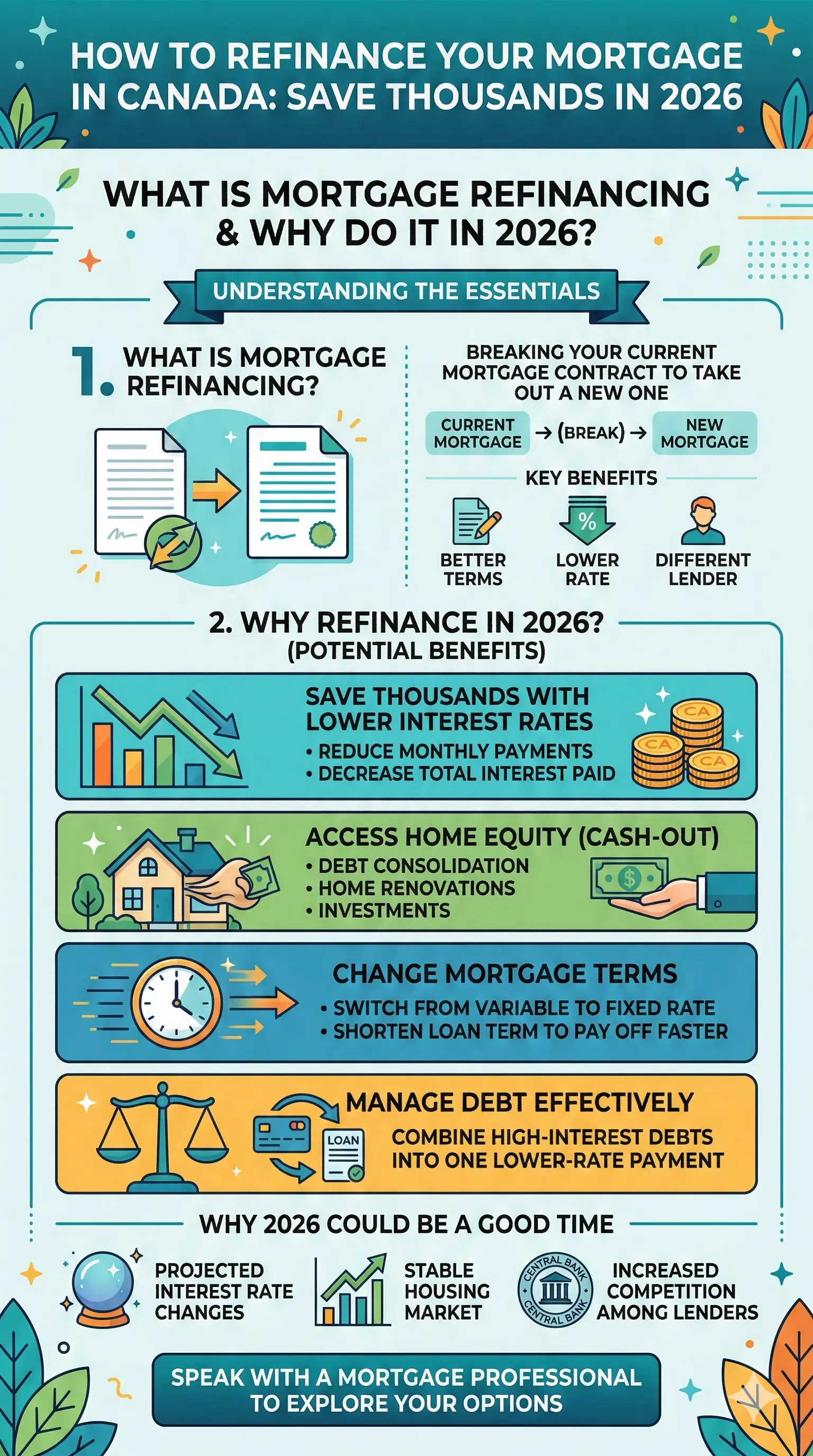

What Is Mortgage Refinancing and Why Do It in 2026?

Mortgage refinancing means replacing your existing mortgage with a new one, often from the same or a different lender. It's not just renewal—it's a chance to renegotiate terms for better rates or cash out equity. In 2026, with many fixed-rate mortgages from low-rate eras expiring, refinancing lets you lock in competitive rates while dodging steep payment jumps.

Key reasons to refinance now:

- Lower your rate: If rates have dropped since your last term, switch to save on interest. Five-year fixed-rate holders renewing in 2026 could see average payment increases of 20% without action.

- Access equity: Pull cash from your home's value for renovations, debt payoff, or investments—up to 90% loan-to-value (LTV) on insured refinances, capped at $2 million homes.

- Shorten or extend amortization: Reduce total interest or ease cash flow; first-time buyers or new builds can go up to 30 years.

- Consolidate high-interest debt: Roll credit card or loan balances into your mortgage at lower rates.

But it's not free—prepayment penalties and fees can eat into savings. Always calculate your break-even point first.

Is Refinancing Right for You? Run the Numbers

Before diving in, assess if refinancing saves money. About 60% of mortgages renewing in 2025-2026 will see payments rise, but smart moves like extending amortization by five years could offset hikes for half of those affected.

Step 1: Calculate Potential Savings

Compare your current rate and payments to new offers. Use online calculators from sites like Rates.ca or WOWA.ca. Factor in:

- Current monthly payment vs. new one.

- Total interest over the term.

- Break-even: Divide total refinancing costs by monthly savings to see months needed to recoup.

Step 2: Check Your Equity and Qualification

You'll re-qualify under OSFI's stress test: prove you can afford payments at the higher of 5.25% or your contract rate plus 2%. Minimum credit score for CMHC-insured refinances is 600. Lenders assess debt service (GDS) and total debt (TDS) ratios—aim for under 39% GDS and 44% TDS.

Pro tip: If you've built equity (common after five years), you might extend amortization from 20 to 25-30 years to lower payments, though this increases lifetime interest.

Understanding Costs: Don't Get Caught Off Guard

Refinancing isn't cost-free. Budget 2-5% of your mortgage principal for fees.

Prepayment Penalties

Breaking a fixed-rate term early triggers an interest rate differential (IRD) penalty—potentially three months' interest or more. Federally regulated lenders follow FCAC guidelines; shop lenders with lower IRDs.

Other Fees

| Fee Type | Typical Cost | Notes |

|---|---|---|

| Appraisal | $300-$500 | Required for equity access. |

| Legal/Transfer | $1,000-$2,000 | Discharge old mortgage, register new. |

| CMHC Premium (if insured) | Up to 4% of loan | Added to mortgage if LTV >80%. |

| Pre-approval/Rate Hold | $0-$500 | Many brokers waive. |

Get a lender payout statement early—it details penalties and discharge fees.

Step-by-Step Guide: How to Refinance Your Mortgage in Canada

Step 1: Review Your Current Mortgage

Check term end date, rate type (fixed/variable), and prepayment rules. Contact your lender for a payout statement.

Step 2: Shop Rates and Lenders

Compare via mortgage brokers (free service) or banks. In 2026, expect 4-5% fixed rates; negotiate against your renewal offer. Use tools like the FCAC rate comparison.

Step 3: Get Pre-Approved

Secure a rate hold (90-120 days). Brokers pull credit once and shop multiple lenders.

Step 4: Gather Documents

- ID (driver's licence, SIN).

- Income proof (T4s, NOAs, paystubs).

- Property docs (title, tax assessment).

- Debt statements.

Use checklists from Mortgages.ca.

Step 5: Choose Options

- Port to new home: Transfer mortgage terms.

- Blend and extend: Mix old/new rates at renewal.

- CMHC Refinance for Suites: Insure up to 90% LTV for secondary suite builds (owner-occupied, $2M cap, 30-year max).

Step 6: Close the Deal

Your lawyer handles funds transfer (1-2 weeks). Funds deposit directly; no cash to you unless equity take-out.

2026 Mortgage Rules Impacting Refinancing

OSFI, CMHC, and federal budgets shape rules. Key 2026 updates:

- 30-year amortizations for first-time buyers/new builds.

- Stress test at contract rate +2% or 5.25%.

- CMHC minimum credit: 600.

- Equity access via HELOCs for short-term relief.

Track changes from OSFI, CMHC, and Finance Canada.

Practical Tips to Maximise Savings

- Work with a broker—access Big 6 banks plus 20+ lenders.

- Time it: Refinance 120+ days before term end to avoid penalties.

- Avoid variable if rates rise; fixed offers stability.

- Pay lump sums at renewal if stress-tested high.

- Consider TFSAs/RRSPs for extra payments tax-free.

Next Steps to Save Thousands Today

Start with your payout statement and a broker consultation—it's free and no-obligation. Compare three offers, crunch numbers, and act before rates shift. With Canada's housing market stabilising in 2026, refinancing positions you for long-term wins. Contact a licensed broker via Mortgage Professionals Canada or use FCAC tools. You'll thank yourself at the lower payments ahead.

Frequently Asked Questions

Sources & References

-

1

Refinancing a Mortgage in Canada: A Checklist — mortgages.ca

-

2

CMHC Mortgage Rules 2026 - WOWA.ca — wowa.ca

-

3

CMHC Refinance for Building Secondary Suites — www.cmhc-schl.gc.ca

-

4

Renewing My Mortgage in 2026 Here's What You Need To Know — www.youtube.com

-

5

How will mortgage payments change at renewal? An updated analysis — www.bankofcanada.ca

-

6

Keeping Track of Mortgage Rule Changes — www.truenorthmortgage.ca