Best Robo-Advisors in Canada 2026: Wealthsimple vs Questrade vs RBC InvestEase

Looking to grow your wealth hands-free in 2026? Robo-advisors like Wealthsimple, Questrade's Questwealth Portfolios, and RBC InvestEase make it easier than ever for Canadians to invest in diversified...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Looking to grow your wealth hands-free in 2026? Robo-advisors like Wealthsimple, Questrade's Questwealth Portfolios, and RBC InvestEase make it easier than ever for Canadians to invest in diversified portfolios without needing a finance degree or constant monitoring.

These platforms use algorithms to build and manage your investments tailored to your goals, risk tolerance, and timeline—perfect for RRSPs, TFSAs, or even FHSA contributions. With low fees, no minimums for some, and access to human support, they're a smart choice amid rising living costs and CRA contribution limits. We'll break down the best robo-advisors in Canada 2026: Wealthsimple vs Questrade vs RBC InvestEase, so you can pick the right one for your portfolio.

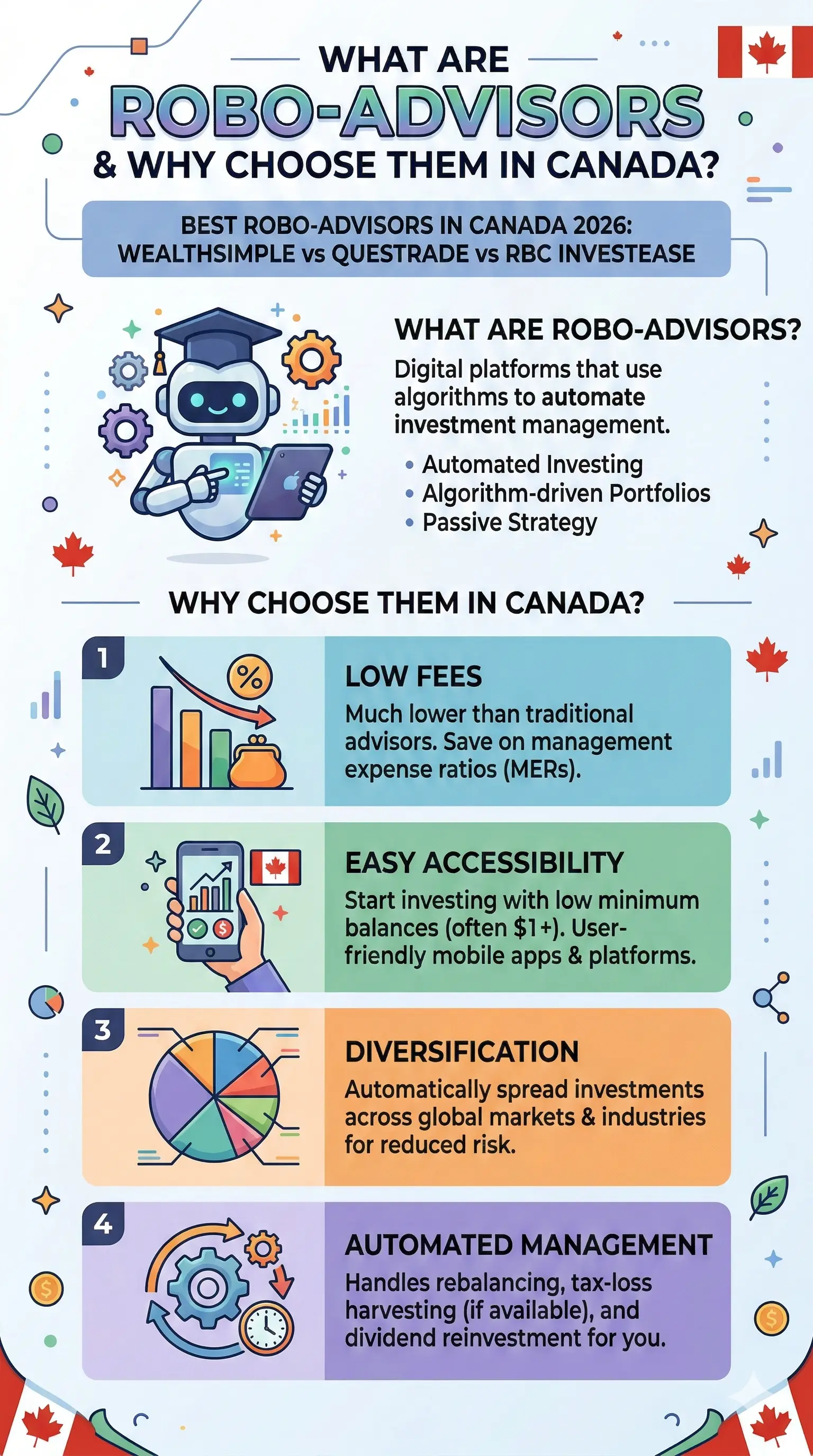

What Are Robo-Advisors and Why Choose Them in Canada?

Robo-advisors automate investing by assessing your profile and creating ETF-based portfolios that rebalance automatically. They're regulated by IIROC and CIRO, ensuring your funds are protected up to $1 million via the Canadian Investor Protection Fund (CIPF). Unlike traditional advisors charging 1-2%, robo fees hover around 0.2-0.7%, saving you thousands over time.

In 2026, with TFSA limits at $7,000 and RRSP deadlines looming, these tools help maximise tax-sheltered growth. They're ideal for beginners, busy professionals, or anyone maximising CPP/EI savings. Key perks include:

- Low entry barriers—no $100K minimums like some advisors.

- Automated tax-loss harvesting to cut your CRA bill.

- Options for ESG or halal investing aligning with Canadian values.

- Integration with bank accounts for seamless transfers.

Wealthsimple: Best Overall for Beginners and Features

Wealthsimple leads as Canada's most popular robo-advisor, often rated best overall for its user-friendly app and zero minimums. Fees range from 0.40-0.50% annually, covering managed accounts with SRI and halal options—great for ethical investing.

Key Features and Fees

- Management Fee: 0.40% on first $100K, dropping to 0.20% on $1M+.

- Minimum: $0 to start—ideal for new savers funding their first TFSA.

- ETFs: iShares, Vanguard for broad exposure (returns ~12-13% over 5 years).

- Support: Phone, chat, and premium human advisors for Pro users.

Wealthsimple shines for its mobile-first design and perks like 1% cashback on spending. In 2026, expect upgraded onboarding and strong performance in volatile markets. Drawback: Slightly higher fees than discount rivals.

Questwealth Portfolios (Questrade): Lowest Fees for Cost-Conscious Investors

Questrade's Questwealth offers some of the lowest fees in Canada at 0.20-0.25%, with no minimum to open (though $1,000 to invest). It's perfect for hands-off investors seeking value, using low-cost ETFs from iShares, BMO, and Global X.

Standout Pros and Performance

| Feature | Details |

|---|---|

| Fees | 0.20% ($100K+), 0.25% (under $100K) |

| Minimum | $1,000 to invest; no account fee |

| Returns (5-yr avg) | ~13.62% |

| Accounts | TFSA, RRSP, RESP, non-registered |

Questwealth suits DIY Questrade users transitioning to managed portfolios. Access investment pros for guidance, and enjoy flat-fee transparency—no hidden MER surprises. It's a top pick for larger balances where savings compound quickly.

RBC InvestEase: Trusted Bank-Backed Option

For RBC loyalists, InvestEase delivers reliability with a big-bank feel. Fees are 0.50% up to $500K (0.40% after), with a $5,000 minimum—backstopped by RBC's 150+ year history.

Why It Fits Canadian Families

- Fees: $4.99/month minimum; scales down for big portfolios.

- ETFs: iShares-focused; strong responsible investing options.

- Returns: Competitive at ~12.45% (5-yr).

- Support: Portfolio advisors for queries, plus RBC app integration.

Great for consolidating TFSA/RRSP/FHSA under one roof, but less flexible for complex needs compared to independents.

Wealthsimple vs Questrade vs RBC InvestEase: Side-by-Side Comparison

| Category | Wealthsimple | Questwealth | RBC InvestEase |

|---|---|---|---|

| Fees (under $100K) | 0.40-0.50% | 0.25% | 0.50% |

| Minimum | $0 | $1,000 | $5,000 |

| Human Support | Yes (premium) | Yes | Yes |

| Best For | Beginners, features | Low fees, value | Bank clients |

| 5-Yr Returns | ~12-13% | 13.62% | 12.45% |

Questwealth wins on fees, Wealthsimple on accessibility, RBC on trust. All offer tax optimisation for CRA filings.

Practical Tips for Choosing and Getting Started

- Assess Your Goals: Use their risk quizzes—match to TFSA for tax-free growth or RRSP for deductions.

- Compare Total Costs: Factor MER (0.1-0.3%) into returns; Questwealth often edges out.

- Test the Platform: Most offer free trials or demos.

- Max Contributions: 2026 TFSA: $7,000; check CRA My Account.

- Rebalance Annually: Review for life changes like buying a home.

Start small: Transfer $1,000 via PAD to see real performance.

FAQ: Common Questions on Canada's Best Robo-Advisors

Which is the cheapest robo-advisor in 2026?

Questwealth at 0.20-0.25%—beats Wealthsimple and RBC for balances over $10K.

Are robo-advisors safe in Canada?

Yes, CIPF protects up to $1M per account. All three are IIROC-regulated.

Can I hold RRSPs and TFSAs?

All support them, plus RESPs (Questwealth) and FHSA (RBC, Wealthsimple).

What's the average return?

10-14% over 5 years, depending on risk—past performance isn't guaranteed.

Do they offer human advice?

Yes: Wealthsimple Pro, Quest pros, RBC advisors—all for complex queries.

Best for ESG investing?

Wealthsimple and RBC InvestEase lead with dedicated portfolios.

Next Steps: Build Your Portfolio Today

Ready to invest smarter? Take Wealthsimple's quiz for ease, Questwealth for savings, or RBC if you're banked there. Open an account in minutes, fund via EFT, and let algorithms handle the rest. Track via apps and adjust as your net worth grows—your future self (and CRA refunds) will thank you. Compare sites directly and start with what fits your 2026 goals.