Self-Employed Taxes Canada 2026: What You Can Deduct and How to File

Running your own business in Canada offers incredible freedom, but it comes with the responsibility of handling your own taxes. For 2026, understanding what you can deduct as a self-employed individua...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Running your own business in Canada offers incredible freedom, but it comes with the responsibility of handling your own taxes. For 2026, understanding what you can deduct as a self-employed individual and how to file correctly can save you thousands while keeping you compliant with the CRA.

Whether you're a freelancer, consultant, or small business owner, maximising your eligible deductions reduces your taxable income and puts more money back in your pocket. We'll break down the top deductions, filing steps, and practical tips tailored for Canadians, using the latest 2026 rules.

Understanding Self-Employed Taxes in Canada for 2026

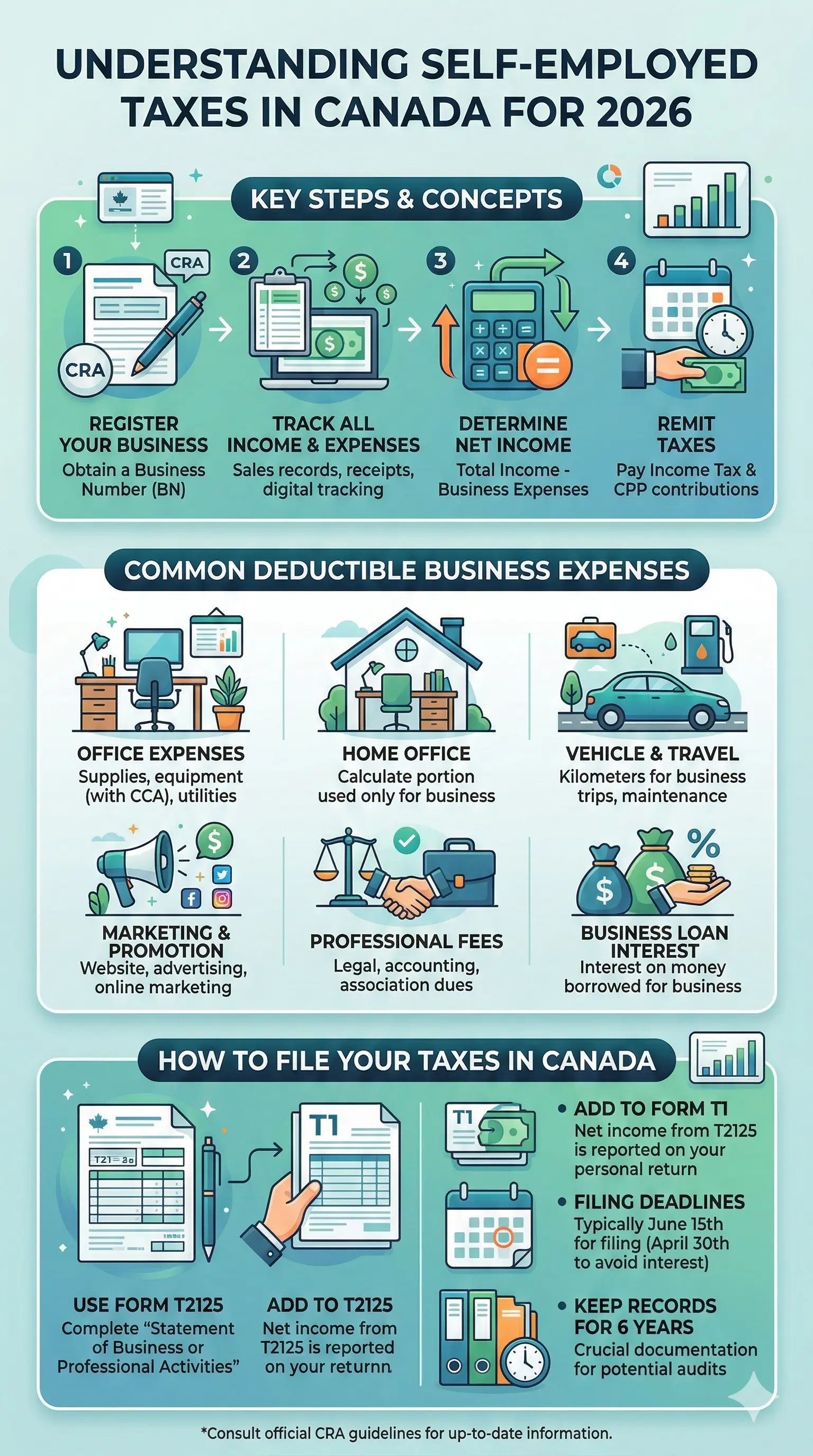

As a self-employed Canadian, you're considered both the employer and employee. This means you pay income tax on your net business income (revenue minus expenses) plus your full share of CPP contributions—up to 11.9% in 2026 on earnings above the basic exemption. Unlike employees, there's no employer withholding taxes from your paycheque, so you'll likely make quarterly instalment payments to avoid penalties.

Key deadlines for 2026 filing (covering your 2025 income):

- April 30, 2026: General filing deadline.

- June 15, 2026: Extended deadline for self-employed individuals.

The cornerstone of self-employed taxes is **Form T2125: Statement of Business or Professional Activities**. This form calculates your net income by subtracting allowable business expenses from your gross revenue.

CPP and EI Contributions for the Self-Employed

In 2026, self-employed Canadians contribute the full CPP amount (employee + employer portions), with a maximum premium of $832.24. Quebec residents use QPP instead. You can opt into EI special benefits for maternity, parental, sickness, or compassionate care, but it's not mandatory.

Tip: Set aside 25-30% of every payment in a separate "tax holding" account to cover income tax, CPP, and potential GST/HST.

Top Deductions for Self-Employed Canadians in 2026

The CRA allows deductions for reasonable expenses incurred to earn business income, but only the business-use portion for mixed items like home offices or vehicles. Here's what you can claim, with real-world examples.

1. Home Office Expenses

If your home is your principal place of business or used exclusively and regularly for client meetings, deduct a portion of eligible costs. For 2026, the CRA retains the simplified deduction: up to $500 without receipts if it's your primary workspace.

Opt for the detailed method for bigger savings—calculate by square footage. Example: If your office is 10% of your home (100 sq ft in a 1,000 sq ft space), deduct 10% of rent ($1,200/month = $120/month), utilities, insurance, and maintenance.

- Eligible: Rent, mortgage interest (not principal), property taxes, utilities, home insurance.

- Not eligible: Mortgage principal, capital improvements, or personal portions.

Documentation: Floor plans, utility bills, photos of workspace. Note: Can't create a loss, but carry forward unused amounts.

2. Vehicle Expenses

Driving to client meetings or supply runs? Deduct based on business-use percentage. Track total km driven (business + personal) via a mileage log—essential for CRA audits.

Choose one method:

- Actual expenses: Gas, insurance, repairs, leasing (business portion only).

- Simplified mileage rate: Check CRA rates for 2026 (typically around 70¢/km for first 5,000 km).

Example: 20,000 km total, 8,000 business km (40%) = deduct 40% of $5,000 annual costs ($2,000 deduction).

3. Office Supplies and Equipment

Pens, printer ink, software subscriptions, and furniture are fully deductible if used for business. For big items like computers (Class 50 CCA), claim depreciation over time via Capital Cost Allowance (CCA).

Bank fees, stamps, and inventory costs also qualify.

4. Phone, Internet, and Utilities

Prorate based on business use. Example: 60% business cell phone = deduct 60% of bill. Same for internet.

5. Advertising, Meals, and Travel

- Advertising: Website, Google Ads, business cards—fully deductible.

- Meals & Entertainment: 50% for client dinners.

- Travel: Flights, hotels (100%), meals (50%) for business trips.

6. Professional Fees and Insurance

Accountants, lawyers, consultants, plus business liability or property insurance—all deductible. Self-employed health premiums via PHSP plans are 100% deductible.

7. Startup Costs and Interest

Initial business setup (up to certain limits) and loan interest for business purposes. Financing fees spread over 5 years (20% annually).

Pro Tip: Use apps like Wave or QuickBooks for tracking—many integrate with CRA's NETFILE.

How to File Your Self-Employed Taxes in 2026

- Gather Records: Receipts, invoices, mileage logs, T4A slips (if commissions).

- Calculate Net Income: Complete T2125. Subtract expenses from revenue.

- Report CPP/QPP: Line 22200 on your T1 return; credit for contributions.

- GST/HST: Register if revenue >$30,000; file separately via NETFILE.

- File Electronically: Use CRA-certified software (TurboTax, H&R Block) or an accountant. Deadline: June 15 for self-employed.

- Pay Instalments: If owing >$3,000 last year, pay quarterly (March 15, June 15, Sept 15, Dec 15).

If hiring employees, deduct their CPP/EI share and remit via payroll.

Practical Tips to Maximise Savings and Avoid Audits

- Separate business/personal bank accounts and credit cards.

- Photograph receipts immediately; use cloud storage.

- Don't mix personal use—prorate accurately.

- Consider incorporating if income >$50,000 for tax deferral (consult a pro).

- Audit defence services like TurboTax's can protect you.

Always keep records for 6 years.

Next Steps for Your 2026 Taxes

Start organising now: Download Form T2125 from canada.ca, track expenses monthly, and estimate instalments using CRA's online calculator. For complex situations, consult a CPA or tax pro—it's often deductible!

Disclaimer: This is general information, not personalised advice. Tax laws change; verify with CRA or a professional for your situation.

Frequently Asked Questions

Sources & References

- 1

-

2

2026 Canadian Tax Updates Every Small Business Should Know — towlerassociates.com

-

3

How to File Self-Employment Taxes in Canada (2026 guide) — www.waveapps.com

-

4

Year-Round Tax Strategies for the Self-Employed in Canada — turbotax.intuit.ca

- 5

-

6

A Guide to Self-Employed Taxes and Rates in Canada — www.wealthsimple.com

-

7

A Simple Guide to Self-Employment Taxes in Canada for 2026 — kataaccounting.com

-

8

What you need to know for the 2026 tax-filing season — www.canada.ca

-

9

Payroll Deduction Tables - 2026 — www.cfib-fcei.ca

-

10

Income tax changes for 2026 — stories.td.com