Best Car Insurance Ontario 2026: How to Stop Overpaying

Are you shelling out hundreds more than you need to on car insurance every year? In Ontario, where average premiums hit $2,006 annually as of late 2024—with GTA drivers facing up to $2,638—you're not...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Are you shelling out hundreds more than you need to on car insurance every year? In Ontario, where average premiums hit $2,006 annually as of late 2024—with GTA drivers facing up to $2,638—you're not alone if you're overpaying.But it doesn't have to be that way in 2026. This guide reveals proven strategies to slash your rates while keeping solid coverage, drawing on Ontario-specific insights and real-world data.

Why Ontario Car Insurance Costs So Much—and How to Fight Back

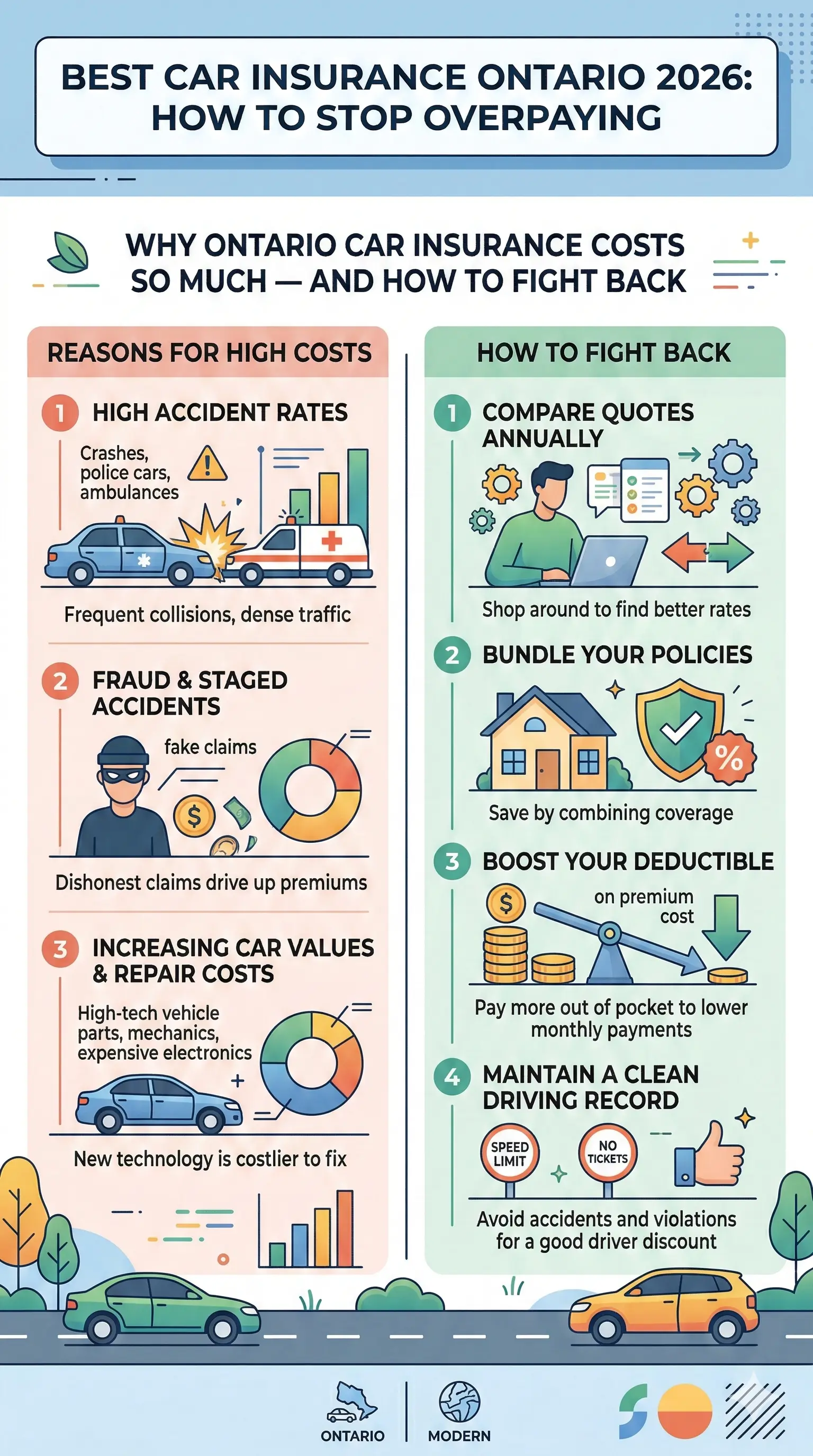

Ontario's private insurance market means premiums vary wildly based on location, driving history, vehicle type, and more.The province boasts some of Canada's highest rates, driven by dense traffic, theft risks, and repair costs. Rural drivers pay around $1,592 yearly, but Toronto-area folks endure steeper hikes.

Factors inflating your bill include:

- Your postal code: Urban spots like the GTA command 60%+ higher premiums due to congestion and crime.

- Driving record: At-fault accidents or tickets can spike rates by 25-50%.

- Vehicle choice: Sports cars or luxury models cost more to insure than safe, compact ones.

- Coverage gaps: Skipping optional perks like direct compensation-property damage (DCPD) might save upfront but expose you later.

The good news? Shopping smart can cut costs by up to 25%, per comparison sites. Start by understanding mandatory coverages under Ontario's Insurance Act: third-party liability (minimum $200,000), accident benefits, uninsured motorist protection, and direct compensation.

Average 2026 Premiums: What to Expect

Expect averages around $2,000-$2,600 yearly, adjusted for 2026 inflation and FSRA rate approvals. New drivers or those in high-risk areas pay more—GTA youth often exceed $3,500. Compare against national benchmarks: Ontario ranks high, but savvy shoppers beat the odds.

Top Strategies to Stop Overpaying in 2026

Don't renew blindly. Here's how to reclaim control:

1. Compare Quotes from Multiple Providers

Ontario's broker model shines here—brokers access dozens of insurers, unlike direct writers limited to one brand. Sites like Ratehub.ca or Surex let you compare in minutes, often saving $600+ yearly.

Action step: Input your details on Ratehub.ca for personalised quotes from Economical, Intact, and more. Aim for 5-10 quotes; the lowest isn't always best—check claims satisfaction via RATESDOTCA's 2026 study.

2. Leverage Discounts Tailored for Ontarians

Stack these to drop premiums 10-30%:

- Multi-vehicle or bundling: Insure home and auto together for 15% off.

- Winter tires: Prove usage for up to 5% savings.

- Anti-theft devices: Factory alarms or trackers qualify for rebates.

- Group rates: CAA members save big; they're often cheapest per Ratehub data.

- Good driver discount: Clean records over 3 years? Expect 35% off.

Brokers like Western Financial Group excel at uncovering these, adapting as your situation changes.

3. Pick the Right Vehicle for Lower Rates

Safety sells. Compact cars with top IIHS ratings keep costs down. Top picks for 2026:

- Honda Civic: Low theft, cheap parts.

- Toyota Corolla: Reliable, high safety scores.

- Hyundai Elantra: Affordable repairs.

SUVs can be budget-friendly too if not luxury models. Avoid high-performance rides—they inflate premiums 20-40%.

4. Time Your Switch Right

Ontario lets you switch anytime without lapse penalties if coordinated properly. Renewals spike in winter—shop 30-60 days early. Use FSRA's rate comparison tools for transparency.

5. Boost Your Profile

Improve credit (insurers factor it), take a defensive driving course via Ontario's Safety League, or install telematics for usage-based insurance—up to 30% off for low-mileage drivers.

Best Car Insurance Providers in Ontario for 2026

No single "best"—it depends on you. Brokers consistently outperform direct buys. CAA tops Ratehub's data for affordability; Intact and Aviva excel in claims.

| Provider | Strength | Avg. Savings Potential |

|---|---|---|

| CAA Insurance | Cheapest overall | Up to 25% |

| Western Financial Group (Broker) | Custom fits | Adaptive rates |

| Economical/Intact | Claims handling | 15-20% |

| Surex Partners | Quick compares | 25% via quotes |

RATESDOTCA's 2026 study ranks by trust and claims; check it annually. For GTA drivers, brokers navigate urban risks best.

Common Mistakes That Keep You Overpaying

- Auto-renewing without shopping: Rates rise 5-10% yearly unchecked.

- Ignoring optional coverages: OPCF 27 (liability waiver) saves post-collision fights.

- Over-insuring old cars: Drop collision if value's low.

- Forgetting principal operator changes: Kids moving out? Update for instant savings.

FAQ

What’s the cheapest car insurance in Ontario for 2026?

CAA often leads per Ratehub data, but compare personally—your rate varies by profile.

Can I switch insurers mid-policy?

Yes, anytime with no gaps. Brokers handle seamlessly to avoid fees.

How much does a ticket affect rates?

Expect 10-25% hikes for minor ones; shop around as not all penalise equally.

Are brokers better than direct insurers?

Usually—access to 20+ companies vs. one, plus free advocacy.

What’s mandatory coverage in Ontario?

$200,000 liability, accident benefits, uninsured motorist, and DCPD.

How do I know if I’m overpaying?

If above $2,000/year outside GTA, compare quotes—you likely are.

Your Next Steps to Save Big in 2026

Grab quotes today via Ratehub.ca or Surex—it's free and takes minutes. Contact a licensed broker for custom advice, and review annually. Track discounts, drive safely, and watch premiums drop. You're now equipped to stop overpaying and drive smarter.