Critical Care and Long-Term Disability Claims Canada: How Insurers Deny and How to Fight Back

Imagine collapsing at work from a sudden stroke, only to have your long-term disability (LTD) claim denied months later because your insurer claims the evidence isn't "objective" enough. This nightmar...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine collapsing at work from a sudden stroke, only to have your long-term disability (LTD) claim denied months later because your insurer claims the evidence isn't "objective" enough. This nightmare is all too common for Canadians facing critical health crises, leaving families scrambling amid medical bills and lost income. In 2026, with rising healthcare costs and complex insurance policies, understanding how insurers deny **critical care and long-term disability claims**—and how to fight back—is essential for protecting your financial future.

Whether you're dealing with cancer, multiple sclerosis, chronic pain, or mental health disorders, private LTD insurance through your employer or individual critical illness policies can be lifelines. But insurers like Manulife, RBC, and Sun Life often reject claims using technicalities. This guide breaks down the process, common denial tactics, and proven strategies to appeal and win in Canada.

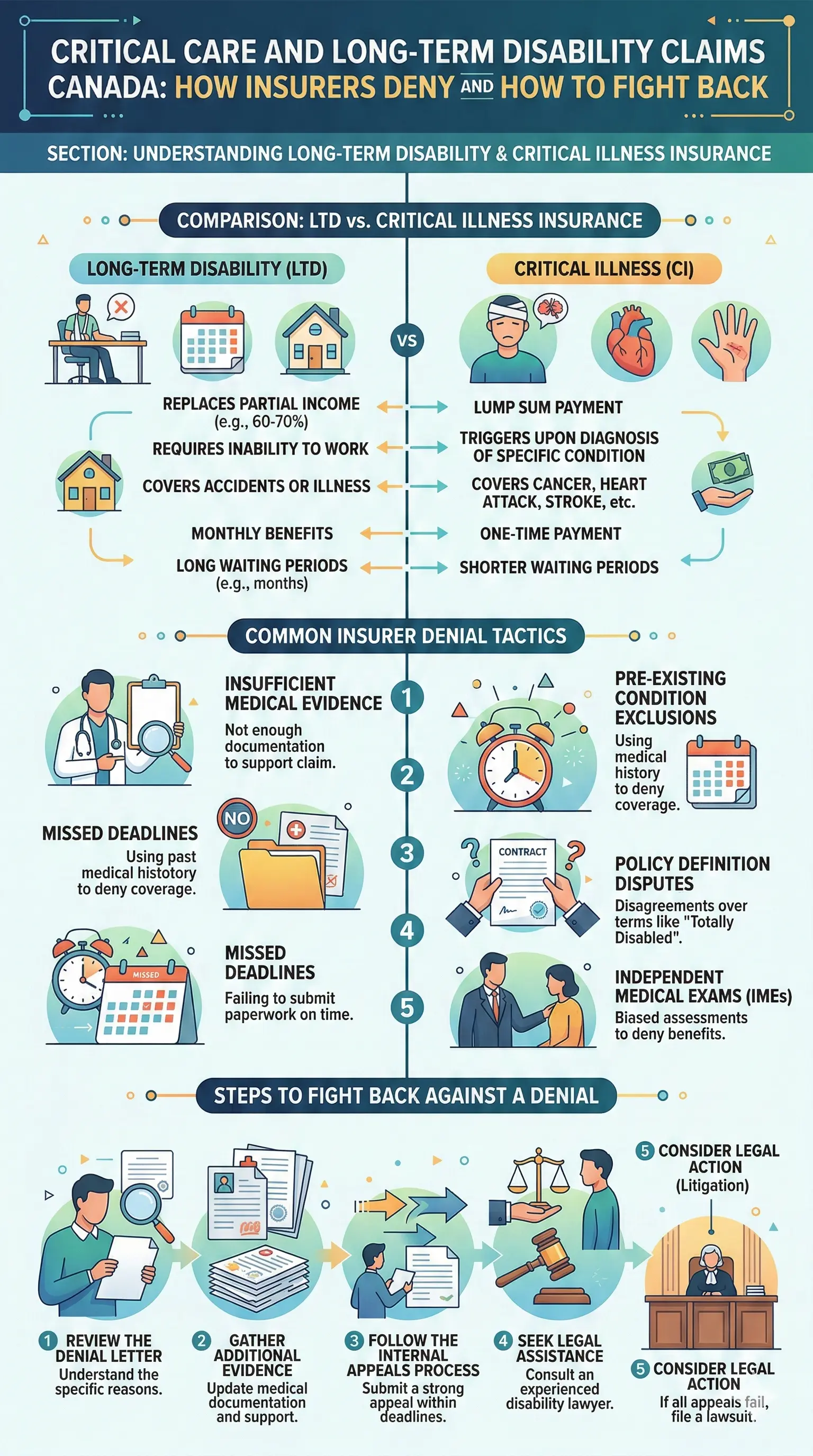

Understanding Long-Term Disability and Critical Illness Insurance in Canada

Long-term disability (LTD) benefits kick in after short-term coverage ends, typically replacing 60-70% of your income if you're unable to work due to illness or injury. Critical illness insurance, meanwhile, pays a lump sum upon diagnosis of covered conditions like heart attack, stroke, or cancer, helping bridge gaps in care or income. Both are vital for Canadians, especially since Canada Pension Plan (CPP) disability benefits average just $1,749 monthly in 2026 and require severe, prolonged conditions.

Key Eligibility Requirements

To qualify for LTD, you must meet your policy's "total disability" definition—often unable to perform your own occupation initially, shifting to "any occupation" after 24 months. Common qualifying conditions include:

- Cancer and neurological disorders like MS, ALS, Parkinson's, or epilepsy, backed by specialist reports and tests.

- Mental health issues such as depression, anxiety, or PTSD, affecting 46% of working-age Canadians with disabilities.

- Musculoskeletal problems and chronic pain, impacting 63% of disabled Canadians per the 2022 Canadian Survey on Disability.

- Critical illnesses covered by policies from providers like Canada Life, Desjardins, or iA Financial.

You'll need Canadian residency, a Disability Tax Credit (DTC) approval in some cases, and recent CRA tax filings. For grave conditions like advanced cancer or ALS, expedited CPP-D processing applies.

The Claims Process: From Application to Waiting Period

Filing an LTD claim starts with your employer statement, attending physician's statement (APS), and medical evidence. Expect a 90-180 day elimination (waiting) period—file at least two months early to avoid gaps. Critical illness claims are simpler: diagnosis triggers payout, but coordination with LTD is key.

Essential Steps for a Strong Application

- Gather Objective Evidence: MRIs, blood work, neuropsychological tests, and specialist reports linking your condition to job duties.

- Complete Forms Accurately: Employer verification of duties and salary; APS detailing limitations.

- Track the Waiting Period: Stay continuously disabled; apply for CPP-D if severe.

- Follow Up: Submit everything promptly to dodge delays.

Pro tip: Provide your doctor with your job description so they connect symptoms—like fatigue from MS or pain flare-ups—to work demands.

How Insurers Deny Critical Care and LTD Claims

Denials hit hard, but they're predictable. Insurers aim to minimize payouts, often citing policy fine print. In 2026, mental health and pain claims face extra scrutiny amid rising claims volumes.

Top 5 Denial Reasons and Examples

- Insufficient Medical Evidence: "Your file lacks objective tests," even with diagnoses. Manulife and RBC often demand specialist reports over GP notes.

- Failure to Meet Waiting Period: Claims rejected if you're not "continuously disabled" for 90-180 days.

- Change in Definition After 2 Years: Benefits cut if you can do "any occupation," not just yours.

- Competing Medical Opinions: Insurer's doctors contradict yours, claiming you can work.

- Inconsistent Treatment: Gaps in records suggest you're not following advice.

"Disability under most policies is about whether you can perform work duties consistently, safely, and reliably—not just diagnosis."

How to Fight Back: Step-by-Step Appeal Guide

Don't give up—most denials are reversible with persistence. Canadian law gives you appeal rights, and limitation periods (often 2 years in Ontario) apply. Act fast to protect deadlines.

Building an Ironclad Appeal

- Review Denial Letter: Identify exact reasons and deadlines (e.g., 60-120 days for internal appeals).

- Gather Stronger Evidence:

- Detailed doctor letters on functional limits (sitting, concentration, flare-ups).

- Vocational assessments proving no suitable jobs exist.

- Daily journals tracking symptoms and failed work attempts.

- File Internal Appeal: Submit within policy timelines, addressing each denial point.

- Seek Legal Help: Disability lawyers offer free consults; many work on contingency (no win, no fee). Firms like Samfiru Tumarkin or UL Lawyers specialize in insurer disputes.

- Escalate if Needed: Sue in court or via ombudsman; rebuild around "reliability" not just diagnosis.

For critical illness denials, verify coverage (e.g., RBC's 25 conditions) and appeal with prognosis updates. Budget tip: Use lump sums for medical gaps, debt, or RRSP/TFSA top-ups.

Practical Tips for Canadians

- Apply for DTC via CRA for tax credits and easier approvals.

- Coordinate with EI sickness benefits (up to $655/week in 2026) during waiting periods.

- Reduce spending: Cut subscriptions, dine out less.

- Document everything—emails, calls, treatments—for your records.

FAQ: Critical Care and Long-Term Disability Claims in Canada

1. What is the typical LTD waiting period in Canada?

90-180 days, averaging 90-120; file early to avoid gaps.

2. Do mental health conditions qualify for LTD?

Yes, depression and anxiety often do, but need detailed APS and treatment records.

3. Can I get CPP disability alongside private LTD?

Yes, but CPP offsets may reduce private benefits; apply for grave conditions ASAP.

4. How long do I have to appeal a denial?

Check policy (often 60-120 days); provincial limits like 2 years apply.

5. Is a lawyer worth it for LTD appeals?

Absolutely—many secure back pay and ongoing benefits on contingency.

6. What if my critical illness claim overlaps with LTD?

Use lump sum for recovery; policies like RBC allow long-term care conversion.

Take Control of Your Claim Today

Facing a denial doesn't mean the end—thousands of Canadians win appeals yearly by arming themselves with evidence and expertise. Start by reviewing your policy, gathering records, and consulting a disability lawyer for a free assessment. Protect your family's security: your health fight deserves financial backing too. Contact resources like Service Canada for CPP-D or CRA for DTC to layer your support.