Critical Illness Insurance Canada: Is It Worth the Premium?

Imagine receiving a diagnosis of cancer or suffering a major heart attack—devastating news that not only upends your health but also your finances. For many Canadians, critical illness insurance offer...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine receiving a diagnosis of cancer or suffering a major heart attack—devastating news that not only upends your health but also your finances. For many Canadians, critical illness insurance offers a financial lifeline, paying a tax-free lump sum to help cover lost income, medical bills, and living expenses during recovery. But with premiums adding to monthly budgets, is it truly worth the cost in 2026?

In Canada, where healthcare covers basics but leaves gaps for non-medical expenses, this coverage is gaining attention amid rising chronic disease rates and healthcare costs. We'll break down what critical illness insurance entails, its benefits and drawbacks, real Canadian claim stats, and practical advice to decide if it's right for you.

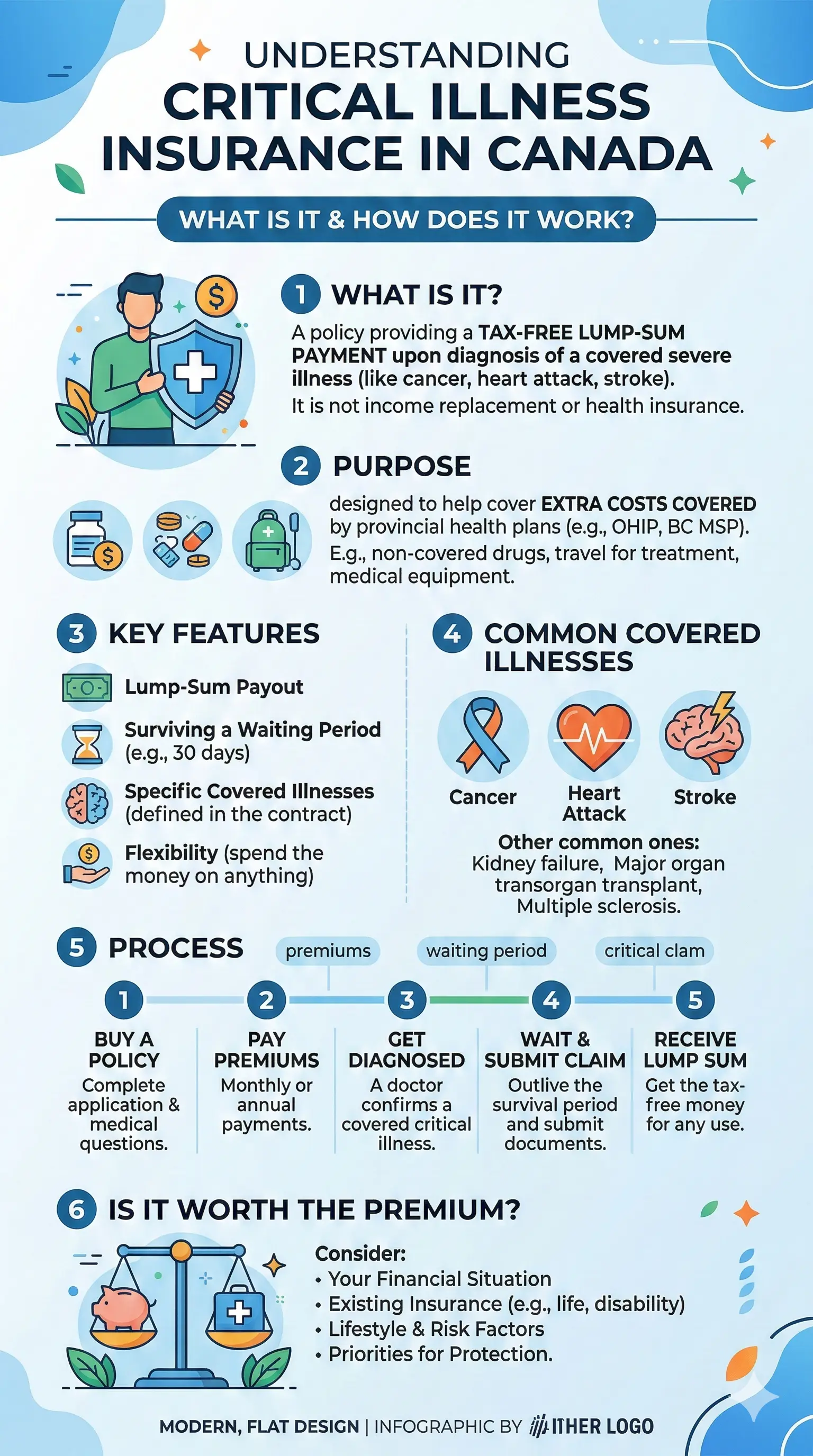

What Is Critical Illness Insurance in Canada?

Critical illness insurance provides a one-time, tax-free payment if you're diagnosed with a covered condition, like cancer, heart attack, or stroke. Unlike health insurance through provincial plans, which handles hospital stays and doctor visits, this policy focuses on your financial recovery.

Policies typically cover 20–25 core conditions, with some extended plans offering up to 120 illnesses, including early-stage cancers for partial payouts. You can spend the money however you need—mortgage payments, childcare, travel for treatment, or even experimental therapies not covered by public health.

How It Differs from Life or Disability Insurance

- Life insurance pays beneficiaries upon death, not during illness.

- Disability insurance replaces income if you can't work, but only monthly and often after a waiting period; it doesn't cover lump-sum needs like home modifications.

- Critical illness delivers immediate cash for any use, even if you keep working.

Only 9% of Canadians have this coverage, despite 57% worrying about serious illness. A common myth? Many think (26% correctly know otherwise) the payout is restricted—it's not.

Why Critical Illness Claims Are Rising in Canada in 2026

Claims are surging due to longer lifespans, better early detection, and persistent chronic diseases. Cancer dominates, accounting for 67–72% of claims and 70% of payouts, followed by cardiovascular issues at 33%.

Rising medical costs amplify the need: Canada's healthcare spending hit $331 billion in 2022 and continues climbing, leaving families vulnerable to out-of-pocket expenses like rehab or family support. Insurers approve 90–95% of valid claims when definitions match, proving reliability if you choose wisely.

Top Covered Conditions and Payout Trends

| Condition | % of Claims | Notes |

|---|---|---|

| Cancer (e.g., breast, lung, prostate) | 67–72% | Includes early-stage partial payouts in modern policies |

| Heart Attack/Stroke | 33% | Core coverage; high approval rates |

| Other (organ failure, neurological) | Remaining | Extended plans cover 20–25+ conditions |

With improved diagnostics, more qualify early, making comprehensive policies essential.

Pros and Cons: Is the Premium Worth It?

The global critical illness market, including Canada, is booming—valued at $330.36 billion in 2026 and projected to reach $621.43 billion by 2030 at 17.1% CAGR—driven by aging populations and healthcare costs. But for individual Canadians, weigh these factors.

Key Benefits

- Financial freedom: Lump-sum payout (e.g., $25,000–$2 million) covers gaps in EI, CPP disability, or RRSP withdrawals.

- Flexibility: Use for anything; 24% don't know claims work while employed.

- Peace of mind: 91% lack it, yet nearly one-third fear savings depletion in six months.

- Return of premium: Some policies refund unused premiums if healthy at term end.

- Multiple claims: Advanced plans allow payouts for recurrent or additional illnesses.

Potential Drawbacks

- Cost: Premiums vary by age, health, and coverage—$20–$100/month for a healthy 30-year-old ($500,000 benefit to age 65). Smokers or those with pre-existing conditions pay more.

- Not guaranteed: Strict definitions (e.g., specific heart attack severity) may deny claims; read fine print.

- One-time payout: No recurrence for same illness unless policy specifies.

- Overlap risk: If you have robust group benefits via employer, it might duplicate.

For many, premiums pale against potential $100,000+ recovery costs. Compare via tools on sites like Kanetix.ca or consult a broker.

Factors to Consider Before Buying in Canada

Assess your situation: family history of cancer? High-risk job? Limited emergency savings? Women and younger Canadians report highest concerns.

Cost Comparison Table (Estimates for Healthy Non-Smoker, 2026)

| Age | Coverage ($500K, Age 65) | Monthly Premium |

|---|---|---|

| 30 | 20-Year Term | $25–$40 |

| 40 | 20-Year Term | $50–$80 |

| 50 | 15-Year Term | $120–$200 |

Rates from broker averages; get personalized quotes. Factor inflation—2026 policies increasingly include CPI indexing.

Shop Canadian providers like Manulife, Sun Life, or RBC Insurance. Check for child riders (covers kids for $10–20K) or spousal add-ons.

Practical Tips for Canadians

- Review provincial health supplements (e.g., BC MSP extras) but note they skip income loss.

- Integrate with TFSA/RRSP for tax-free growth on payouts.

- Buy young: Lock in low rates before health changes.

- Use online calculators from Insurance Bureau of Canada (IBC).

- Compare 3–5 quotes; prioritize high claim payout ratios (90%+).

FAQ: Critical Illness Insurance Canada

1. Does critical illness insurance cover mental health conditions?

No, standard policies focus on physical illnesses like cancer or stroke. Some emerging plans add neurological coverage.

2. Can I get a payout if I return to work?

Yes, it's a lump sum regardless of employment status—only 24% of Canadians know this.

3. What's the waiting period?

Typically 90–180 days post-diagnosis; survival required (e.g., 30 days).

4. Is it worth it if I'm healthy?

Absolutely for high earners or families; stats show 91% unprotected despite risks.

5. How does it interact with government benefits?

Tax-free and independent of EI/CPP; use to bridge gaps without clawbacks.

6. Are premiums tax-deductible?

No for individuals; possibly for self-employed via CRA rules—check cra-arc.gc.ca.

Next Steps: Secure Your Financial Health Today

Critical illness insurance isn't for everyone, but with cancer claims at 67% and 91% of Canadians exposed, it's a smart hedge against life's uncertainties. Start by calculating your needs: tally six months' expenses, add debt, and subtract savings.

Consult a licensed advisor via Advocis or IBC.ca. Get quotes from multiple insurers, focusing on definition clarity and return-of-premium options. Protect your family's future—act before premiums rise with age.