Disability Insurance Canada: Protecting Your Income When You Can't Work

Imagine waking up one day unable to work due to a sudden illness or injury, watching your savings dwindle while bills pile up. For Canadians, **disability insurance** offers a vital safety net, replac...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine waking up one day unable to work due to a sudden illness or injury, watching your savings dwindle while bills pile up. For Canadians, **disability insurance** offers a vital safety net, replacing a portion of your income when you can't earn it yourself—yet many remain underinsured in 2026.

This protection is especially crucial as living costs rise and chronic health issues like mental health disorders drive more claims. Whether you're self-employed, a professional, or relying on employer plans, understanding **Disability Insurance Canada** can safeguard your financial future.

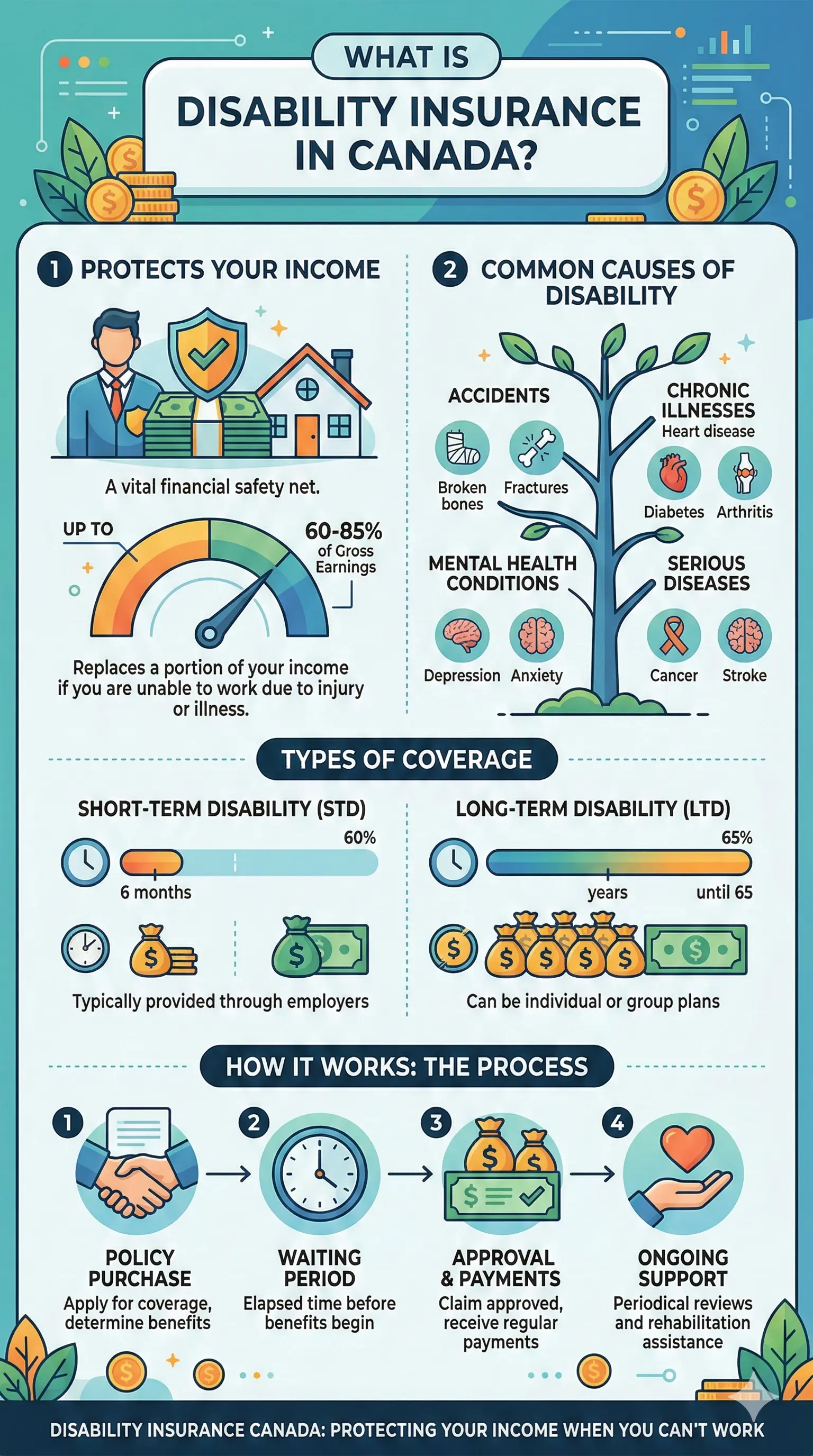

What Is Disability Insurance in Canada?

Disability insurance, also known as income protection insurance, provides monthly payments if an illness, injury, or accident prevents you from working. It typically replaces 60-90% of your pre-disability income, helping cover essentials like mortgage payments, groceries, and utilities.

Unlike life insurance, which pays out after death, disability coverage focuses on your earning years. Policies define disability in two main ways:

- Own occupation: Can't perform your specific job (preferred for professionals).

- Any occupation: Can't work in any job suited to your skills (more common, cheaper premiums).

In Canada, this insurance bridges gaps left by government programs, which often fall short for maintaining your lifestyle.

Types of Disability Insurance Available

Canadians have several options tailored to their needs:

- Individual policies: Bought directly from insurers like Canada Life, Manulife, or RBC Insurance—portable and customizable.

- Group/employer-sponsored: Often basic, covering 60% of income; ends if you leave your job.

- Professional association plans: Affordable for doctors, lawyers, or accountants via groups like Edge Benefits.

Top providers in 2026 include Canada Life, RBC Insurance, Manulife, Desjardins, and Humania, offering flexible riders for inflation protection or partial disability.

Why You Need Disability Insurance in 2026

Nearly 1 in 3 Canadians will face a disability lasting over 90 days before age 65, yet a 2025 survey showed only 25% of self-employed workers have coverage—compared to over half with employer benefits. With an aging workforce and rising chronic conditions, the risks are higher than ever.

Government benefits like CPP Disability ($1,741 maximum monthly in 2026 for highest earners) or the Canada Disability Benefit (just $200/month max) replace only a fraction of income. Working-age Canadians with severe disabilities have a median after-tax income of $30,590—far below the $46,080 average—pushing poverty rates to 18%.

The Disability Risk Is Real for Canadians

- Mental health claims now dominate, alongside musculoskeletal issues.

- Self-employed professionals (e.g., consultants, gig workers) lack EI sickness benefits beyond 15 weeks.

- Longer careers mean higher exposure; premiums rise with age but protect longer.

Without coverage, you risk depleting RRSPs/TFSAs early, accruing debt, or delaying retirement. Disability insurance ensures continuity.

Government Disability Benefits vs. Private Insurance

Canada's public safety nets are limited—here's how they stack up:

| Benefit | Max Monthly Amount (2026) | Eligibility | Coverage Level |

|---|---|---|---|

| CPP Disability | $1,741 (highest) | Severe, prolonged disability; contributions required | ~30-40% of income |

| Canada Disability Benefit | $200 | Disability Tax Credit holder; low income | Minimal supplement |

| EI Sickness | 55% of earnings (up to $695/week) | Short-term (15 weeks); insurable employment | Temporary only |

| Private Disability Insurance | 60-90% of income | Own/any occupation; health underwriting | Comprehensive, long-term |

Note: CPP figures are quarterly averages indexed for 2026. Private insurance fills the gap, often coordinating with these to avoid overpayment.

How Much Does Disability Insurance Cost in Canada?

Premiums average 1-3% of annual income—about $40-$125/month for low-risk profiles. Costs depend on age, occupation, health, benefit amount, waiting period (30-90 days), and duration (to 65 or 70).

Sample Premiums for 2026 (35-Year-Old Male, Non-Smoker, $5,000 Monthly Benefit to Age 65)

| Waiting Period | Monthly Premium |

|---|---|

| 60 Days | $100.94 |

| 90 Days | $83.00 |

By age (90-day wait, $5,000 benefit):

- 25: $62

- 35: $83

- 45: $131

- 55: $223

Higher-risk jobs like truck driving cost more (~$128/month). Shop around—quotes vary by provider.

Key Features to Look for in a Policy

Customize your plan with these essentials:

- Benefit period: To age 65 (standard) or 70 for late retirees.

- Waiting period: Longer = lower premiums; pair with EI/CPP.

- Riders: Cost-of-living adjustment (COLA), future increase option, partial disability.

- Non-cancelable: Locks in rates/premiums.

- Residual benefits: Pays proportionally if working reduced hours.

For self-employed, ensure portability and tax-deductible premiums via CRA rules.

Steps to Get Disability Insurance in Canada

- Assess needs: Calculate 60-90% of net income; factor in debts, family support.

- Check existing coverage: Employer/group plans, CPP eligibility.

- Get quotes: Compare 3-5 providers (e.g., PolicyAdvisor tools).

- Undergo medical exam: Disclose health history honestly.

- Apply and review: Confirm own-occupation definition; add riders.

- Pair with RDSP: If eligible, use 2026 matching grants (up to $3,500/year for low-income).

Act early—premiums rise with age and health changes.

FAQ: Disability Insurance Canada

Is disability insurance tax-free in Canada?

Yes, benefits are tax-free if premiums are paid with after-tax dollars (personal policies). Employer-paid may be taxable.

What's the difference between short-term and long-term disability?

Short-term (STD): 3-6 months, often employer-provided. Long-term (LTD): Years to retirement, via private insurance.

Can I get disability insurance if self-employed?

Absolutely—individual policies are ideal. Only 25% of self-employed have it, but it's essential without EI.

How long does approval take?

2-6 weeks, including medical underwriting. Faster for healthy applicants.

Does mental health qualify for claims?

Yes, increasingly common (e.g., depression, anxiety); ensure policy covers psychiatric conditions.

What if I have a pre-existing condition?

Disclosure required; coverage may exclude it or rate higher. Buy young and healthy.

Protect Your Income Today

Don't leave your finances to chance—**disability insurance** is your strongest defence against income loss. With government benefits covering just a sliver of needs, private coverage ensures you keep your lifestyle intact.

Next steps:

- Calculate your coverage gap using online tools.

- Contact providers like Manulife or Canada Life for free quotes.

- Consult a broker via PolicyAdvisor for personalized advice.

- Explore RDSP if eligible for long-term savings.

Secure your policy now and gain peace of mind for whatever lies ahead.