Condo Insurance Canada 2026: Why Your Building Policy Isn't Enough

Imagine coming home to find your condo flooded from a burst pipe, your cherished furniture ruined, and a neighbour's unit damaged below yours. Your condo corporation's master policy covers the buildin...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine coming home to find your condo flooded from a burst pipe, your cherished furniture ruined, and a neighbour's unit damaged below yours. Your condo corporation's master policy covers the building's structure, but who pays for your soaked belongings, temporary hotel stays, or potential lawsuits? In Canada, relying solely on your building's insurance leaves you dangerously exposed—this is why personal condo insurance is essential in 2026.

With rising condo prices, frequent extreme weather, and increasing legal claims, understanding condo insurance Canada 2026 gaps is crucial for every owner. We'll break down why the building policy falls short, what your personal policy must cover, and practical steps to protect yourself financially.

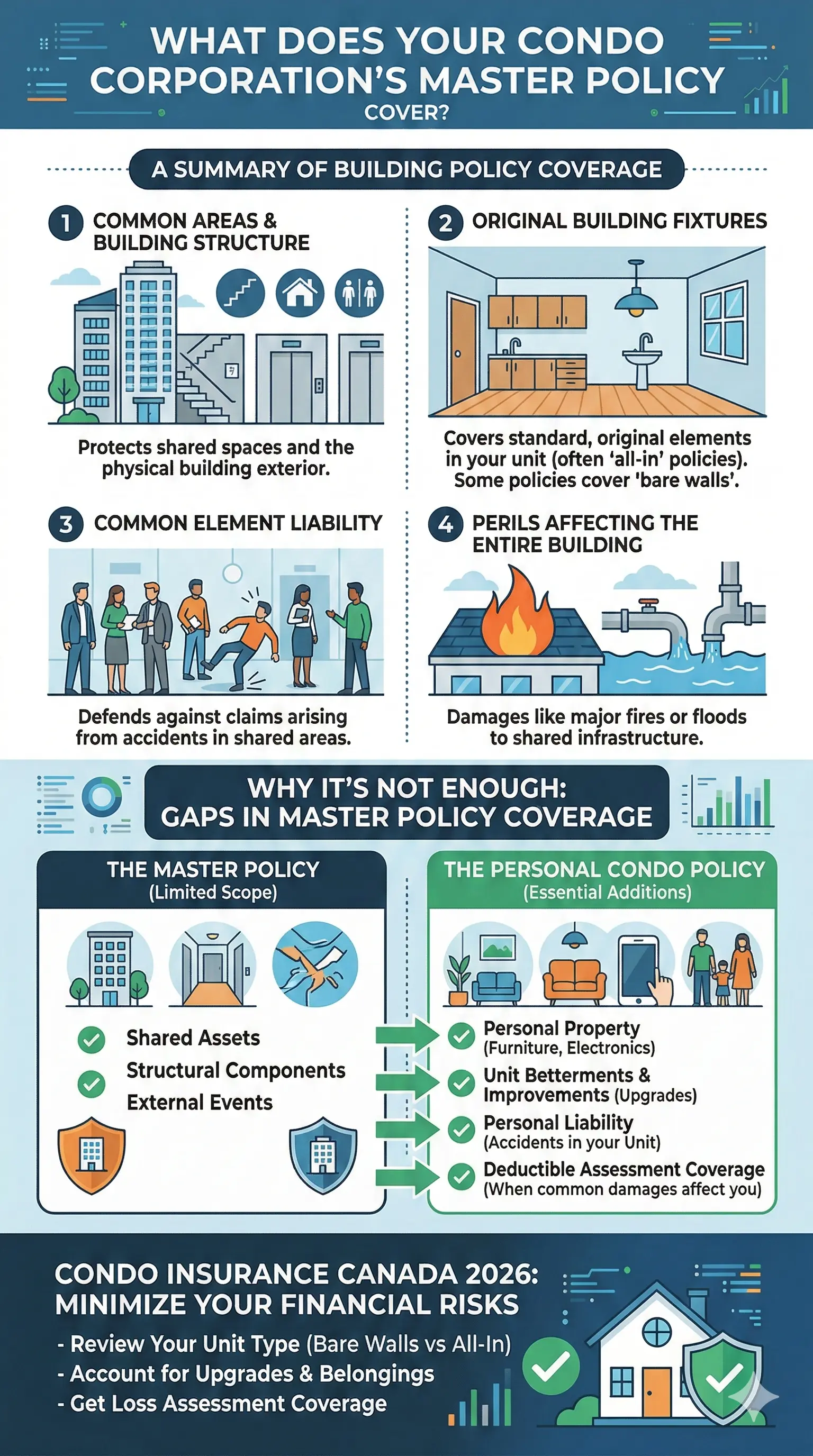

What Does Your Condo Corporation's Master Policy Cover?

Every condo corporation in Canada must maintain a master insurance policy under provincial laws, like Saskatchewan's Condominium Property Act, 1993, which requires coverage for common property, facilities, and the building structure at full replacement value against major perils. This includes walls, roofs, elevators, and shared hallways, often with high liability limits—some providers now start at $30 million to handle catastrophic claims.

However, these policies have limitations. They typically exclude your unit's interior improvements, personal belongings, and liability arising from your space. In high-risk areas, add-ons like flood, hail, earthquake, or water damage might be included, but deductibles can be steep, and coverage doesn't extend to your private contents.

Key Gaps in Master Policies

- Standard Unit Document (SUD) Boundaries: Coverage stops at the unfinished surfaces of your unit (bare walls, floors, ceilings). Anything beyond—like custom flooring or cabinetry—is your responsibility.

- No Personal Property: Furniture, electronics, clothing, and valuables in storage lockers aren't covered.

- Limited Liability: While the corporation insures common areas, you're liable for incidents inside your unit.

- High Deductibles and Assessments: If claims exceed limits, owners share costs via special assessments—up to $500,000 minimum in some basic policies.

Condo bylaws often mandate personal insurance to fill these gaps, and mortgage lenders require proof before approving loans, even though it's not legally required by any province.

Why Personal Condo Insurance Is Non-Negotiable in 2026

Home insurance isn't mandatory by law anywhere in Canada, but for condo owners, it's practically essential due to bylaws, lenders, and real risks like water damage—the top claim source. A basic HO-6 policy (standard for condos) protects what the master policy misses: your contents, upgrades, liability, and extra living costs.

In 2026, with climate change driving more floods and storms—especially in Quebec and BC—minimum coverage won't cut it. Many associations now demand $2 million in personal liability, up from $1 million, as accidents in high-rises can cascade damages quickly.

Essential Coverages in Your Personal Policy

Review your policy against these must-haves:

| Coverage Type | Minimum Limit (2026 Recommendation) | What It Protects |

|---|---|---|

| Personal Belongings | $30,000 minimum; aim for $100,000+ | Theft, fire, or damage to clothes, tech, furniture. |

| Physical Structure & Fixtures | $500,000 minimum | Interior walls, plumbing, built-ins within your unit. |

| Renovations/Betterments | $500,000 minimum; match your upgrades | Custom kitchens, flooring beyond SUD. |

| Personal Liability | $2 million recommended | Injuries or damage you cause to others. |

| Additional Living Expenses | $50,000 minimum; up to $5M via corp add-ons | Hotels if uninhabitable. |

| Loss Assessment | $500,000 minimum | Shared corp costs exceeding master limits. |

Add-ons like deductible buy-down (to reduce your share of corp deductibles), third-party liability, and flood/earthquake riders are wise, especially in flood-prone areas like Ontario or BC.

Real-Life Risks: Canadian Condo Insurance Claims in 2026

Water leaks cause most claims, but fires, theft, and weather events are rising. A kitchen overflow could cost thousands in neighbour damages—not covered by the master policy. In large Toronto or Vancouver towers, one incident might trigger multi-unit claims, hitting your liability fast.

Surveys show 19% of owners don't realise two policies are needed, and half ignore corp deductibles they might owe pro-rata. In Quebec, with harsh winters, freeze damage is common, amplifying the need for robust coverage.

Provincial Nuances

- Ontario/Saskatchewan: Strict bylaws reference SUD; annual master policy reviews required.

- BC/Alberta: Strata plans demand high liability; earthquake coverage key.

- Quebec: Syndicates handle buildings, but co-owners need personal policies for contents.

How Much Does Condo Insurance Cost in Canada 2026?

Average premiums range $300–$800 annually for basics, rising with location, building claims history, and limits. Opt for $2M liability to meet bylaws—it's often just $50–$100 more yearly. Shop via brokers for tailored quotes, bundling with auto for discounts.

Practical tip: Use Statistics Canada's consumer price index for insurance (up 5% in 2025) to budget; get quotes from providers like YouSet or BFL Canada.

Actionable Steps to Get Proper Coverage

- Review Bylaws & SUD: Know your corporation's requirements and unit boundaries.

- Inventory Belongings: Appraise valuables; photograph for claims.

- Upgrade Limits: Boost liability to $2M, add ALE and loss assessment.

- Check Add-Ons: Flood, earthquake, bylaw coverage for 2026 risks.

- Shop Annually: Compare 3–5 quotes; ask about corp extensions like directors' liability.

- Proof of Insurance: Provide to lenders and strata immediately.

Consult the Insurance Bureau of Canada (IBC) for provincial guides at ibc.ca.

Protect Your Condo Lifestyle Today

Don't let gaps in coverage turn a mishap into financial ruin. In 2026's unpredictable climate, a solid personal condo policy alongside your building's master insurance ensures peace of mind. Start by reviewing your bylaws, inventorying assets, and getting quotes—your future self will thank you.

Next steps: Contact a licensed broker, visit canada.ca insurance page for tips, or use IBC tools to compare.

Frequently Asked Questions

Sources & References

-

1

Condo Protection Program | Condo Corporations | BFL CANADA — www.bflcanada.ca

- 2

-

3

Is home insurance mandatory in Canada? | Westland Insurance — www.westlandinsurance.ca

-

4

Understanding Condominium Insurance Requirements — www.mckercher.ca

-

5

The Ultimate Guide to Condo Insurance: Everything You Need to Know — www.cayugamutual.com

- 6