Canada GST/HST for E-Commerce Businesses 2026: What Online Sellers Must Know

If you're running an e-commerce business in Canada, understanding GST/HST rules isn't optional—it's essential. Whether you're selling digital products, physical goods, or services online, the Canada R...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're running an e-commerce business in Canada, understanding GST/HST rules isn't optional—it's essential. Whether you're selling digital products, physical goods, or services online, the Canada Revenue Agency (CRA) expects you to collect and remit the correct tax. Get it wrong, and you're facing penalties, interest charges, and potential audits. Get it right, and you'll keep your business compliant whilst staying competitive. Let's break down what you need to know in 2026.

Understanding GST/HST Registration Requirements

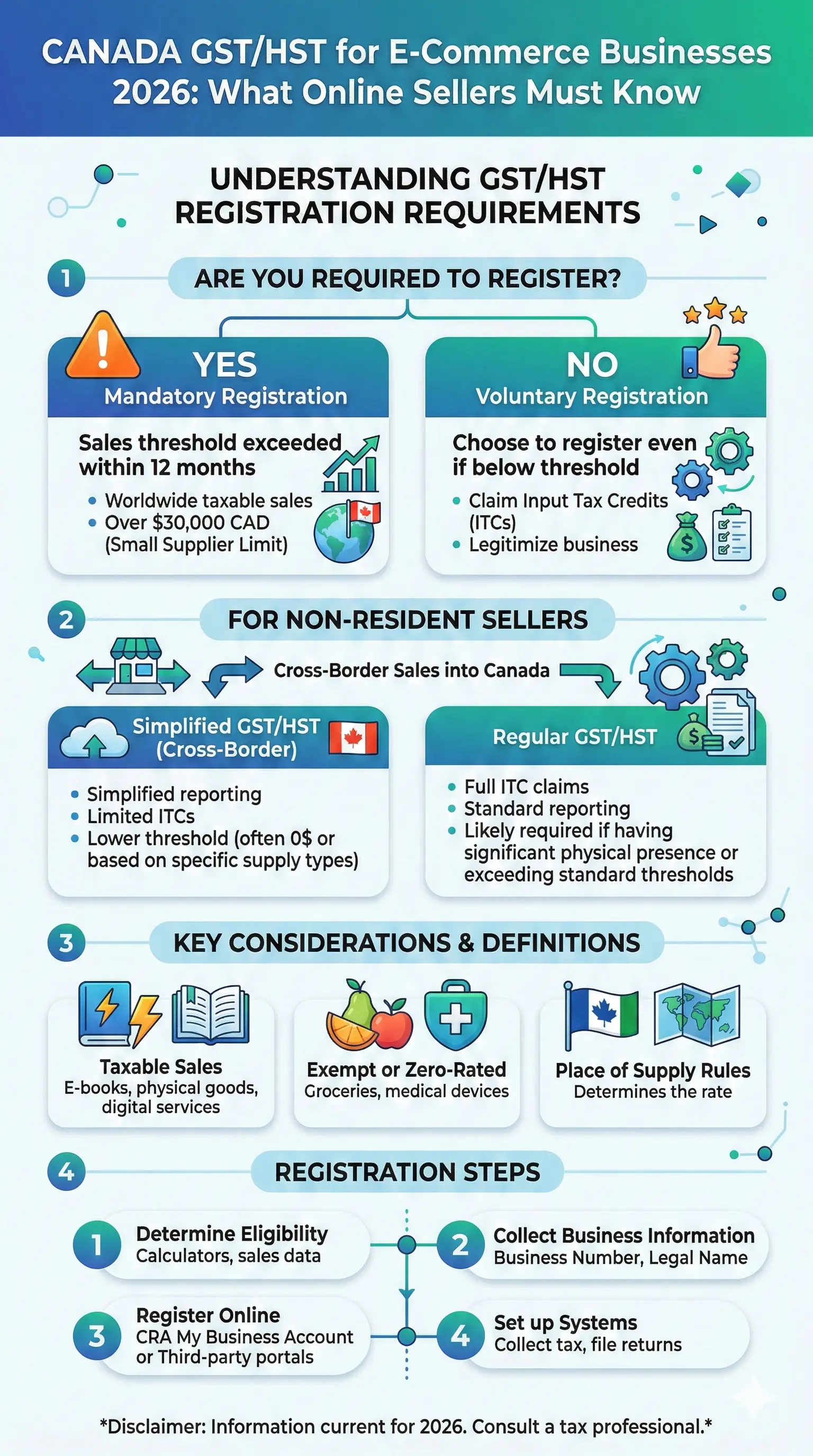

The first question every online seller asks is: "Do I need to register for GST/HST?" The answer depends on your sales volume and business type.

When Registration Is Mandatory

If your worldwide taxable supplies exceed $30,000 in any four consecutive calendar quarters, you must register for GST/HST within 29 days of exceeding the threshold. This applies regardless of where you're located—whether you're based in Canada or operating as a foreign vendor selling to Canadian customers.

This $30,000 threshold is crucial. Many e-commerce businesses don't realize they've crossed it until the CRA contacts them. Keep careful records of your sales, because exceeding this threshold triggers a legal obligation to register.

Voluntary Registration Benefits

Even if you're below the $30,000 threshold, you can register voluntarily. Why would you do this? The main advantage is claiming input tax credits (ITCs) on your business expenses. If you're investing heavily in inventory, software, or marketing, recovering GST/HST paid on these costs can significantly improve your cash flow.

However, there's a catch: if you register under the simplified system (which applies to certain non-resident vendors), you cannot claim ITCs. This is an important distinction that affects your overall tax position.

GST/HST Rates Across Canada in 2026

Tax rates vary by province, and this complexity is where many e-commerce businesses stumble. You need to charge the correct rate based on your customer's location, not your own.

Here's what you're working with:

- GST only (5%): Alberta, British Columbia, Northwest Territories, Nunavut, Saskatchewan, Yukon

- HST (13%): Ontario, Newfoundland and Labrador, Nova Scotia, Prince Edward Island, New Brunswick

- HST (15%): None currently (Nova Scotia reduced from 15% to 13%)

- GST + PST: British Columbia, Saskatchewan, Manitoba

- GST + QST (14.975%): Quebec

For physical goods, charge tax based on the delivery address. For digital products and services, charge tax based on the customer's location (typically their billing address or IP address). Your e-commerce platform should be configured to automatically apply the correct rate—most modern platforms like Shopify handle this automatically if you set it up properly.

Digital Products and Services: Special Rules

If you're selling digital products or online services, there are specific rules you need to follow.

What Counts as Taxable Digital Products?

Software, e-books, music, videos, and other digital downloads are all taxable. The place of supply is the customer's location, which means you must:

- Collect tax based on the customer's province

- Verify customer location properly

- Not charge tax on exports (sales outside Canada)

Online Services and SaaS

SaaS platforms, cloud services, consulting delivered online, and similar digital services are taxable based on customer location. Subscription services are taxed monthly or annually, whilst one-time services are taxed at the time of delivery. B2B services may have different rules, so consult with a tax professional if you're selling to businesses.

Non-Resident Vendors: The Simplified Registration System

If you're a non-resident vendor (not carrying on business in Canada) supplying digital products or services to Canadian consumers, you may qualify for the simplified registration system. This system was introduced July 1, 2021, and applies to supplies made on or after that date.

Here's the critical difference: under simplified registration, the GST/HST you collect is not eligible for input tax credits. This means you can't recover GST/HST paid on your business expenses in Canada. For many businesses, this makes simplified registration less attractive than regular registration, but it may still be your only option depending on your circumstances.

Physical Goods and Fulfillment Warehouses

If you're selling physical products to Canadian customers, the rules depend on where your inventory is stored.

Goods Shipped from Canada

If you use a fulfillment warehouse in Canada to store and ship goods to Canadian customers, you may need to register under the normal GST/HST system (not the simplified system). This applies even if you're a non-resident vendor. The key trigger is that goods are located in a fulfillment warehouse in Canada or shipped from a place in Canada to a purchaser in Canada.

Third-Party Fulfillment Providers

If you use a third-party fulfillment provider in Canada, that provider must already be registered for GST/HST and is required to notify the CRA that they're carrying on this business. They must also maintain records regarding their non-resident clients and the goods they store on their behalf. This is important—if you're using a fulfillment warehouse, confirm they're CRA-registered and compliant.

The 2026 Import Changes: What's Different

Starting in 2024 (continuing through 2026), Canada eliminated the low-value exemption for imports. GST now applies to almost all imports, ending old exemptions for postal shipments under CAD 40. This means:

- GST applies to shipments under CAD 20 for duties and varying tax thresholds

- Couriers are fully taxed (no exemptions)

- E-commerce platforms like Shopify must handle collection for remote sellers

If you're importing goods to resell in Canada, you'll need to factor GST into your landed costs. Use apps for landed cost calculations and consider DDP (Delivered Duty Paid) shipping terms to simplify the process.

USMCA Benefits for US and Mexican Suppliers

If you're importing qualifying goods from the US or Mexico under the USMCA (United States-Mexico-Canada Agreement), you may qualify for low or zero duties. However, documentation must be perfect—you'll need origin certificates to prove eligibility. For high-volume shippers, the savings outweigh the administrative burden.

Compliance and Record-Keeping

The CRA takes e-commerce compliance seriously. Here's what you need to do:

- Keep detailed records: Document all sales, tax collected, and business expenses for at least six years

- File GST/HST returns: File quarterly or annually, depending on your registration status and sales volume

- Maintain invoices: Your invoices must show the GST/HST amount clearly

- Track customer locations: For digital products and services, document how you determined customer location

Non-compliance can result in significant penalties and interest charges. If you're audited and found to have under-collected or under-remitted tax, you'll owe the full amount plus penalties.

Frequently Asked Questions

Do I need to register if I'm just starting my e-commerce business?

Not necessarily. You only need to register once your sales exceed $30,000 in any four consecutive calendar quarters. However, registering voluntarily early can help you claim ITCs on startup costs, which may benefit your cash flow.

How do I determine a customer's location for digital products?

Use their billing address or IP address. Most e-commerce platforms can automatically detect location based on IP address, but billing address is the most reliable method. Document your process for CRA compliance.

Can I claim input tax credits if I register under the simplified system?

No. Under the simplified registration system for non-resident vendors, GST/HST collected is not eligible for ITCs. This is a significant disadvantage, so consider whether regular registration is possible for your business.

What happens if I don't register when I'm required to?

The CRA can assess you for unpaid GST/HST, plus penalties and interest. You could also face operational disruptions if audited. It's far better to register proactively once you exceed the threshold.

Do I charge GST/HST on exports outside Canada?

No. Sales outside Canada are not subject to GST/HST. Make sure your e-commerce platform is configured to recognize international customers and not charge Canadian tax.

How often do I need to file GST/HST returns?

This depends on your registration status and sales volume. Most businesses file quarterly, but some may file annually. Check with the CRA or a tax professional for your specific requirements.

Next Steps for Your E-Commerce Business

Getting GST/HST right doesn't have to be complicated, but it does require attention to detail. Here's what you should do now:

- Calculate your sales: Track your worldwide taxable supplies over the past four calendar quarters to determine if you've exceeded the $30,000 threshold

- Register with the CRA: If you're required to register, do so within 29 days of exceeding the threshold. Visit canada.ca for registration information

- Configure your platform: Ensure your e-commerce platform is set up to charge the correct GST/HST rates by province and customer location

- Consult a professional: If you're selling digital products, using fulfillment warehouses, or importing goods, consider consulting a tax accountant familiar with e-commerce compliance

- Keep records: Implement a system to track sales, tax collected, and business expenses for CRA audits

The e-commerce landscape in Canada is evolving, but the fundamentals remain the same: understand your obligations, collect the right tax, and keep good records. By staying compliant in 2026, you'll protect your business and compete fairly with other Canadian sellers.