Best Home Insurance in Canada 2026: What's Covered and What's Not

Owning a home in Canada is a major milestone, but protecting it from the unexpected—like wildfires in British Columbia or basement flooding in Ontario—requires the right home insurance. With average a...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Owning a home in Canada is a major milestone, but protecting it from the unexpected—like wildfires in British Columbia or basement flooding in Ontario—requires the right home insurance. With average annual premiums around $1,300 in 2026, choosing the best home insurance in Canada means balancing coverage, cost, and reliability to safeguard your biggest investment.

This guide breaks down top providers, what’s typically covered (and what’s not), and practical tips to get the most value, so you can shop confidently across provinces.

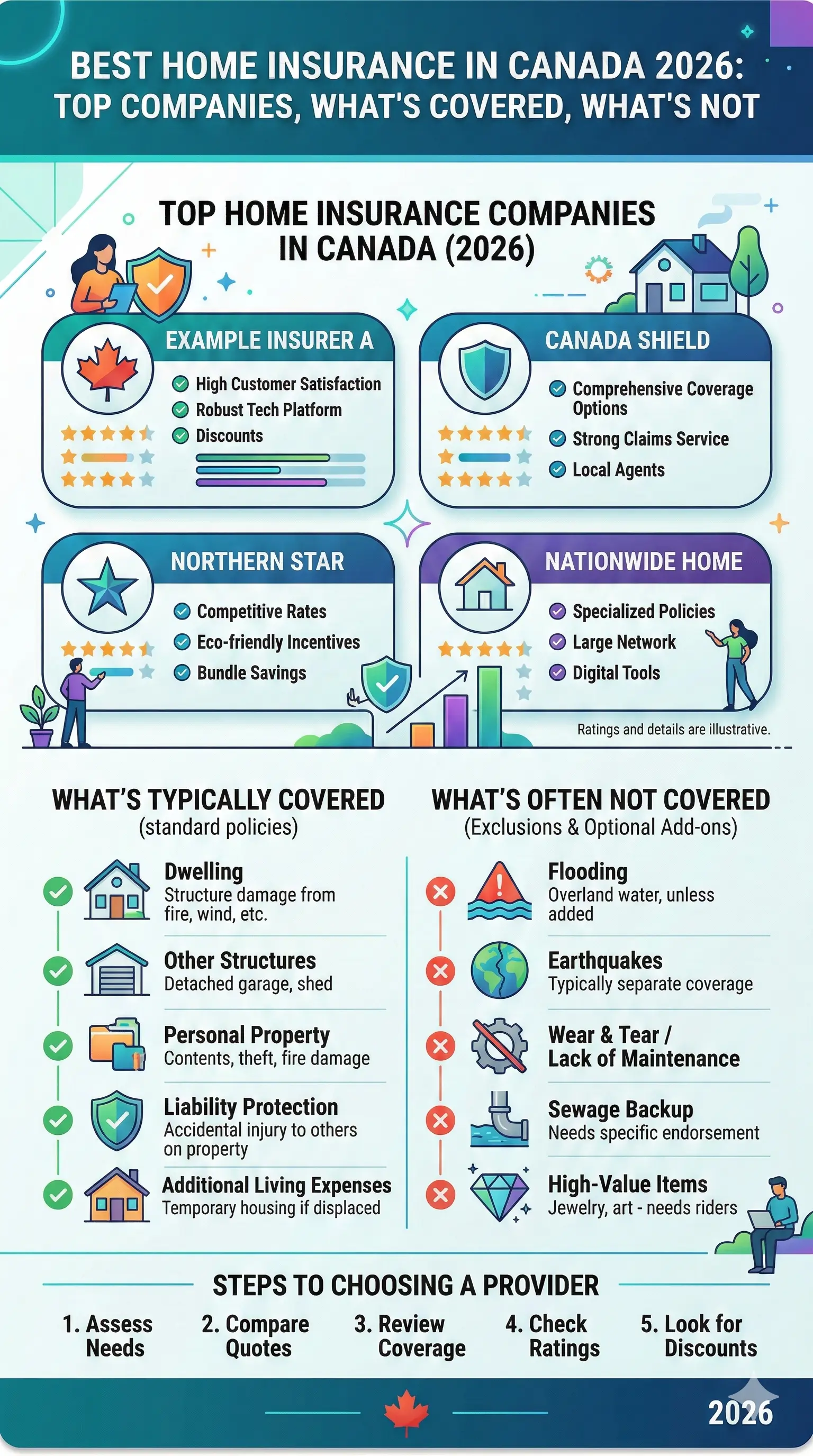

Top Home Insurance Companies in Canada for 2026

Canada’s home insurance market is competitive, with rankings from J.D. Power and broker surveys highlighting customer satisfaction in claims, pricing, and service. Providers like Intact, Aviva, and Desjardins consistently top lists for their nationwide reach and strong performance.

J.D. Power's Top-Ranked Providers

J.D. Power evaluates insurers on non-claim interactions, price, policy offerings, billing, and claims handling—key for real-world peace of mind. Their latest rankings name these as Canada’s best:

- Intact Financial Corporation: Largest provider with over $20 billion in premiums; excels in custom packages for all provinces.

- Aviva Canada: Covers 860,000+ homes; strong in Ontario with flexible add-ons like identity theft protection.

- Desjardins General Insurance: Cooperative model shines in Quebec and Ontario; average premium $1,280 with upgrade discounts.

- Wawanesa Mutual Insurance: Budget-friendly at $1,280/year; praised for efficient claims.

- Economical Insurance: Flexible policies averaging $1,320; top in Ontario per user ratings.

Best by Province

Provincial differences matter—Alberta faces hail risks, while Quebec has lower premiums around $768/year historically. Here’s a snapshot:

| Province | Top Providers |

|---|---|

| Ontario | Square One (A), Economical (A), Intact (A) |

| Alberta | RSA (A), Intact (A-), Economical (A-) |

| Quebec/Ontario | Desjardins |

| B.C. | Intact, Aviva (highest premiums ~$924) |

Digital options like Sonnet ($1,300 average) suit tech-savvy Canadians in Ontario, Quebec, and Atlantic provinces with instant quotes.

What’s Covered in Canadian Home Insurance Policies?

Standard policies in Canada follow the Insurance Bureau of Canada (IBC) framework, offering three main types: basic (named perils), broad, and comprehensive (all-risk). Coverage splits into dwelling (structure), personal property, and liability.

Core Coverages You’ll Get

- Dwelling and Other Structures: Rebuilds your home, detached garage, or shed after fire, windstorm, or hail. Extended replacement cost covers rising 2026 rebuild costs amid inflation.

- Personal Property: Protects belongings like furniture against theft or damage; often 50-70% of dwelling limit.

- Additional Living Expenses (ALE): Hotel costs if your home is uninhabitable post-claim.

- Liability: $1-2 million+ for guest injuries or property damage you cause.

- Personal Liability: Covers legal fees if your dog bites a neighbour.

Average premiums reflect risks: $1,280-$1,350 nationally, higher in B.C. ($924) and Alberta ($912).

Common Add-Ons for Better Protection

Enhance basics with these, especially in flood-prone areas:

- Overland Water Protection: Basement flooding from heavy rain—essential post-2025 storms.

- Sewer Backup: Clogged drains; pairs with water coverage.

- Earthquake: Critical in B.C. or Ottawa Valley.

- Identity Theft: Offered by Aviva.

What’s Not Covered? Key Exclusions to Watch

No policy covers everything—knowing exclusions prevents claim denials. Standard gaps include:

- Flooding from Outside Sources: Rivers or oceans; buy separate flood insurance via IBC partners.

- Earthquakes and Mine Subsidence: Add riders; not in basic policies.

- Wear and Tear, Pests, or Mould: Maintenance issues like rot or rodent damage.

- High-Risk Items: Jewellery over $2,000 or bikes need schedulers.

- War, Nuclear, or Intentional Damage: Obvious exclusions.

- Business Use: Home offices may void coverage without endorsement.

In Quebec, civil code requires proof of insurable interest; elsewhere, provinces mandate minimum liability via laws like Ontario’s Insurance Act.

How to Choose the Best Home Insurance for Your Needs

Compare quotes from at least three providers—use tools like WOWA.ca or LowestRates.ca for side-by-side views. Factor in:

Practical Tips for Canadians

- Get Multiple Quotes: Online from Sonnet or Desjardins; brokers for bundled home-auto savings (10-15%).

- Bundle Policies: Save with TD or Aviva on home + auto.

- Check Discounts: Multi-policy (15%), claims-free (10%), or upgrades like alarms (5%). Wawanesa excels here.

- Assess Risks: B.C. homeowners add wildfire; Prairies need hail coverage.

- Review Annually: Update for renovations or inflation—2026 rebuild costs up 5-7%.

Work with brokers for negotiation power, as My Insurance Broker offers.

FAQ: Common Questions on Home Insurance in Canada 2026

What’s the average cost of home insurance in Canada? Around $1,300/year, varying by province—lowest in Quebec (~$768), highest in B.C. (~$924).

Is home insurance mandatory in Canada? Not federally, but most mortgages require it. Provinces like Ontario enforce via lenders.

Does home insurance cover floods? No, standard policies exclude overland flooding; add separate coverage.

Can I insure a rental property? Yes, via landlord policies from Intact or Co-operators.

How do I file a claim? Contact your insurer immediately—Aviva and Wawanesa process fast digitally.

What if I work from home? Declare it for business endorsement to avoid voids.

Next Steps to Secure Your Coverage

Start by gathering home details (square footage, build year, renovations) and requesting quotes from top picks like Intact, Desjardins, or Sonnet today. Compare via a licensed broker for free, and review policy wordings for exclusions. With Canada’s weather patterns intensifying, comprehensive coverage now protects your family and finances tomorrow—shop smart for 2026 peace of mind.

Related Articles

Wood Stove and Fireplace Home Insurance Rules in Canada 2026

There's something undeniably special about the warmth and ambience of a wood stove or fireplace in a Canadian winter. However, that crackling fire comes with a set of insurance rules that many homeown...

Airbnb and Short-Term Rental Insurance in Canada 2026

Thinking about listing your home on Airbnb or Vrbo can be exciting, but it also raises an important question: does your standard home insurance policy cover short-term rentals? For most Canadians in 2...

Home-Based Business Insurance in Canada 2026: When Does Your Home Policy Stop Covering You?

Picture this: you’ve started a small side hustle from your home office—perhaps freelance graphic design, online tutoring, or selling handmade crafts on Etsy. You feel confident knowing your home insur...

How to Get the Best Home and Auto Insurance Bundle Discount in Canada 2026

If you’re a homeowner with a car, you’ve almost certainly seen the ads promising big savings if you bundle your home and auto insurance with the same provider. But is it really worth it? In 2026, with...