Best Mortgage Brokers in Canada 2026: Broker vs Bank — Who Gets You a Better Rate?

Are you staring down a mortgage decision in 2026, wondering if a broker or your bank will land you the best deal? With Canadian home prices stabilising after recent volatility and interest rates holdi...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Are you staring down a mortgage decision in 2026, wondering if a broker or your bank will land you the best deal? With Canadian home prices stabilising after recent volatility and interest rates holding steady around 4-5% for prime borrowers, choosing between a mortgage broker and a bank could save you thousands over your loan term.

In this guide, we'll break down the key differences, spotlight top performers, and arm you with practical tips to secure the lowest rates—tailored for Canadians navigating the current market.

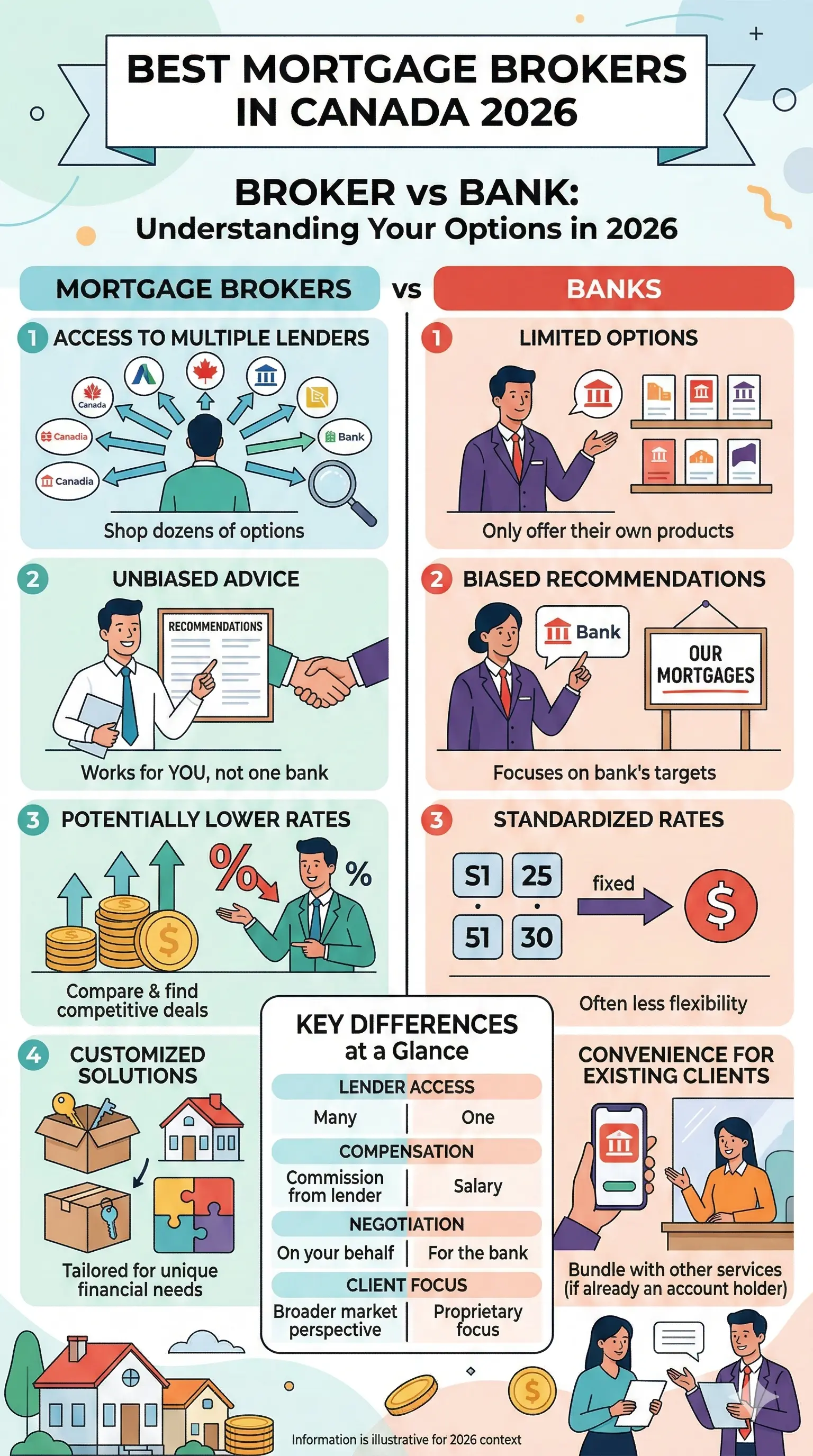

Broker vs Bank: Understanding Your Options in 2026

Mortgage brokers act as independent shoppers, comparing offers from multiple lenders like banks, credit unions, and private financiers, often accessing over 30 institutions at once. Banks, on the other hand, only offer their own products, which might suit you if you're already a loyal customer with a strong relationship.

Under Canada's Bank Act and oversight from the Financial Consumer Agency of Canada (FCAC), both options are regulated, but brokers provide a free service—paid by lenders via commissions—making them a no-cost way to shop around.

How Brokers Work: Your Personal Mortgage Shopper

Brokers like True North Mortgage, Canada's largest independent brokerage, connect with big banks, credit unions, and non-bank lenders such as First National Financial to find tailored deals. They handle paperwork, negotiations, and even complex cases like self-employed borrowers or new-to-Canada immigrants.

- Access to exclusive rates not available directly to consumers.

- One-stop shopping: Compare dozens of options without multiple credit checks.

- Expertise in niches like refinance, renewals, or investor mortgages.

Bank Mortgages: Convenience with Limits

Major banks like RBC Royal Bank, Scotiabank, BMO, and CIBC dominate with national branches and digital tools, offering perks like bundled accounts or rewards programs. For 2026 refinances, RBC leads with HELOC options, while Tangerine provides competitive digital rates due to low overhead.

However, banks prioritise their in-house products, potentially limiting flexibility for non-standard profiles.

Who Gets You a Better Rate? The Data Speaks

In 2026, brokers often edge out banks on rates by 0.2-0.5%, thanks to volume deals and competition among lenders. Ratehub.ca, a top brokerage, has funded over $15 billion since 2015, boasting 4.9/5 stars from 10,000+ reviews by securing optimal terms.

| Factor | Mortgage Broker | Big Bank |

|---|---|---|

| Average Rate Savings | 0.2-0.5% lower | Standard posted rates |

| Lender Access | 30+ (banks, credit unions, non-banks) | 1 (their own) |

| Cost to You | Free | Free, but less negotiation |

| Best For | Complex needs, first-time buyers | Loyal customers, simple deals |

For example, Homewise, ranked Canada's top broker, leverages 30+ lenders for competitive edges, while First National Financial—Canada's largest non-bank lender—partners exclusively with brokers.

Best Mortgage Brokers in Canada for 2026

We've curated top brokers based on volume, reviews, and 2026 performance from industry rankings like Canadian Mortgage Professional's Top 75 Brokers.

Top National Brokerages

- True North Mortgage: Largest independent broker with 30+ lender partnerships. Ideal for refinances and custom solutions.

- Ratehub.ca: Fastest-growing, ex-bank experts handling everything from first-time buys to divorce mortgages. 4.9/5 rating.

- Homewise: Smooth process, top-ranked for 2026 with broad lender access.

Standout Individual Brokers

From MPA Magazine's 2024 Top 75 (updated rankings expected for 2026):

- Collin Bruce, Dominion Lending Centres: Top small-market performer.

- Kirk Bryan, The Genesis Group: High-volume expertise.

- Scott H. Bentley, Mortgage Centre Canada: Resilient in tough markets.

These pros excel by personalising advice beyond rates, like equity release for renovations or pre-retirement planning.

Best Banks for Mortgages in 2026

While brokers shine for variety, banks remain strong for reliability:

- RBC Royal Bank: Widest refinance options, national presence.

- Tangerine Bank: Digital-first, competitive rates.

- Scotiabank: Negotiable rates for existing clients.

- BMO: 900+ branches, hybrid digital/in-person.

- CIBC: Flexible tools for all Canadians.

Largest non-bank lenders like EQB and First National often route through brokers for better access.

Practical Tips: Securing the Best Rate in 2026

Boost your approval odds and snag lower rates with these Canadian-specific steps:

- Check your credit score via Equifax or TransUnion—aim for 680+ for prime rates.

- Compare using tools from Ratehub.ca or FCAC's pre-approval guide (canada.ca).

- Time your renewal: Shop 120-180 days early to avoid default rates up to 2% higher.

- Leverage CMHC insurance for down payments under 20%—brokers navigate this seamlessly.

- Ask about cash-back or rate holds amid Bank of Canada fluctuations.

"Working with a mortgage broker is completely free—they're paid by the lender—and gives access to the best rates from a variety of sources."

FAQ: Mortgage Brokers vs Banks in Canada

1. Are mortgage brokers free in Canada?

Yes, brokers earn commissions from lenders, so there's no cost to you.

2. Can brokers get better rates than banks?

Often yes, by comparing 30+ lenders versus a bank's single offering—savings of 0.2-0.5% are common.

3. What's the best broker for first-time buyers?

Ratehub.ca or Homewise excel here, with expertise in CMHC-insured mortgages.

4. Do banks offer exclusive perks?

Yes, like rewards or bundled chequing, but brokers can match or beat rates.

5. How do I switch mid-term?

Refinancing via brokers like True North is straightforward, especially with equity.

6. Are there regional differences?

Brokers access national lenders, but local credit unions via brokers suit smaller markets.

Next Steps: Find Your Best Mortgage Today

Start by getting pre-approved—contact top brokers like Ratehub.ca or True North for a free comparison, or chat with your bank. Use FCAC's mortgage calculator at canada.ca to model scenarios. In 2026's market, proactive shopping ensures you don't overpay. Reach out to a licensed broker today; your future self (and wallet) will thank you.