Mortgage Rates Canada 2026: Fixed vs Variable — What Experts Say Now

As we navigate 2026, Canadian homeowners and buyers face a pivotal choice: fixed or variable mortgage rates? With the Bank of Canada holding its policy rate steady at 2.25% amid sticky inflation and e...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

As we navigate 2026, Canadian homeowners and buyers face a pivotal choice: fixed or variable mortgage rates? With the Bank of Canada holding its policy rate steady at 2.25% amid sticky inflation and economic uncertainty, experts predict stability for most of the year—but potential upticks loom. This guide breaks down the latest forecasts, compares your options, and shares what top economists are saying to help you decide confidently.

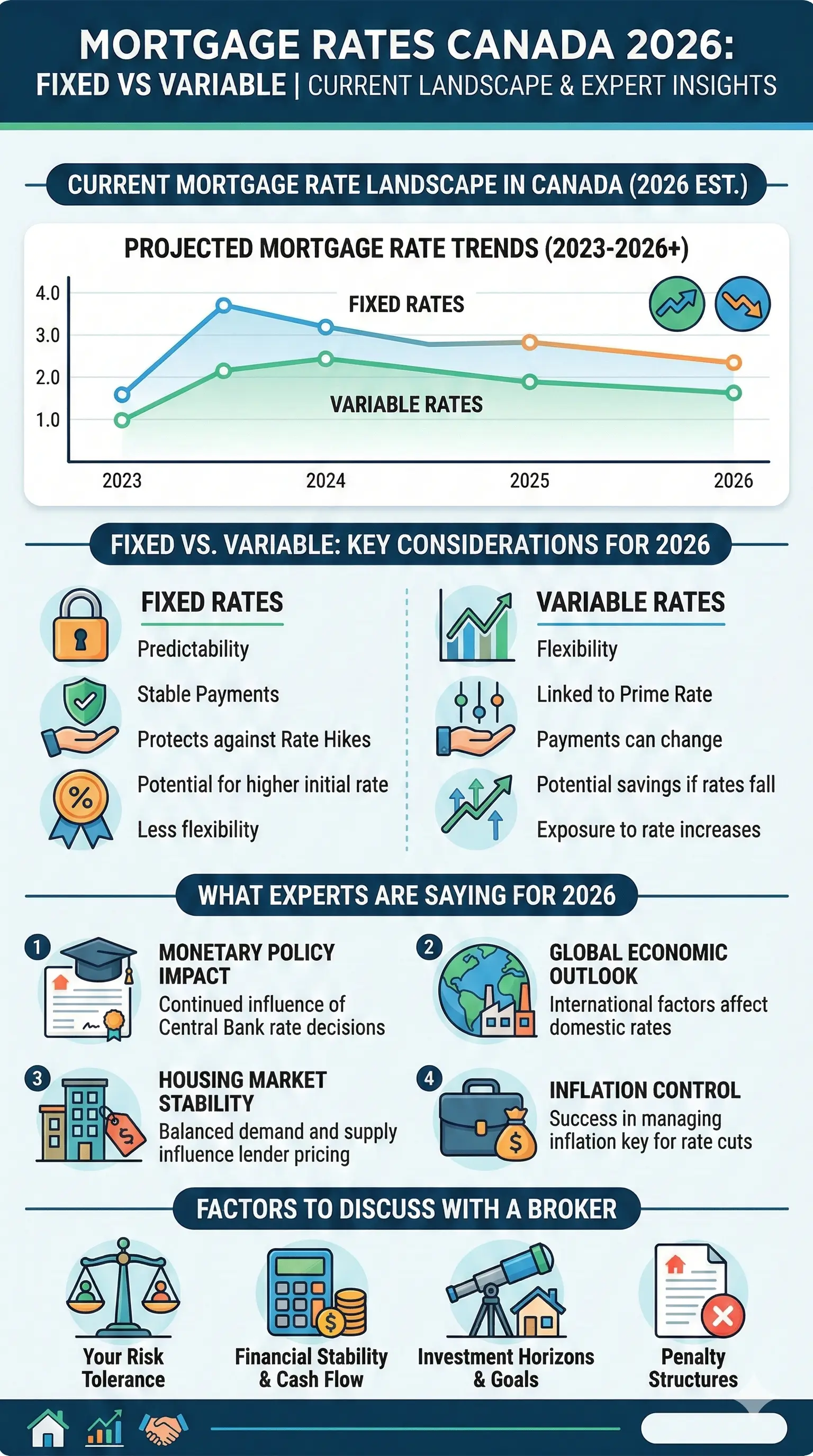

Current Mortgage Rate Landscape in Canada for 2026

The Bank of Canada has kept its overnight policy rate at 2.25% since late 2025, with the prime rate steady at 4.45%. This pause reflects balanced inflation around 2.2-2.4% headline and higher core measures at 2.5-2.8%, as the central bank monitors global trade tensions and domestic job softness.

Advertised mortgage rates range from 3.69% to 6%, with a realistic benchmark around 4.2% depending on term, credit, and lender. For an average $520,000 mortgage (based on a $670,000 home with 20% down), this translates to monthly payments of roughly $2,500-$3,000, varying by amortisation and type.

Bank of Canada Rate Decisions Shaping 2026

After cuts in 2025, the BoC announced no changes on January 28, 2026, citing appropriate policy amid uncertainty. Forecasts from major banks diverge slightly:

- RBC and TD expect stability at 2.25% through 2026.

- Scotiabank and National Bank predict a 0.5% rise by year-end to 2.75%.

- BMO and CIBC see it holding at 2.25%, with hikes possibly in 2027.

Bond yields, which drive fixed rates, suggest little further decline, while variable rates track the prime directly.

Fixed vs Variable Mortgage Rates: Key Differences

Fixed rates lock in your payment for the term (typically 1-5 years), offering predictability. Variable rates fluctuate with the prime rate, potentially saving money if rates fall but risking hikes.

| Feature | Fixed Rates | Variable Rates |

|---|---|---|

| 2026 Forecast | Stable near 4.5%; slight rise possible | Stable at prime-linked 3.95-4.45%; potential +0.5% |

| Risk Level | Low (payments fixed) | Medium (payments may adjust) |

| Best For | Budget certainty, renewals from low rates | Risk-tolerant buyers expecting holds/cuts |

| Current Best Rates | ~4.2-4.5% (5-year) | ~3.95% (prime -0.5% discounts) |

Fixed Mortgage Rates in 2026: Stability with Upside Risks

Five-year fixed rates are projected to hover near 4.5% through 2026, unlikely to drop further as bond markets price in the status quo. For the 33% of borrowers renewing in 2026—mostly from 5-year fixed pandemic-era deals—payments could jump 20% on average due to higher rates.

"Fixed rates are expected to rise slightly, while variable rates remain broadly stable until mid-2026."

CMHC notes fixed options provide shelter from volatility, ideal if you're renewing soon.

Variable Mortgage Rates: Holding Steady, But Watch for Hikes

Variable rates, tied to prime (4.45%), offer discounts like 0.5% off, hitting 3.95% for strong applicants. With BoC on hold, payments stay flat for now—but experts warn of hikes if inflation persists. Adjustable payment variables could see changes if prime rises to 4.95%.

What Experts Say: Fixed or Variable in 2026?

Economists urge caution over optimism. Nesto's Q4 2025 survey shows consensus on 2.25% BoC rates, but with rate-hike probabilities rising. Mortgage Sandbox predicts asymmetric risk: no big drops, but inflation could push fixed up and variables higher.

- RBC Economics: Hold at 2.25% in 2026; upside from U.S. policies.

- TD Economics: Steady through 2027; no rush to variable.

- True North Mortgage: BoC at 2.50% by end-2026; favour fixed for renewals.

- Perch CEO Alex Leduc: No movement in 2026; prepare for 2027 hikes.

75% of renewing fixed borrowers face shocks—experts recommend stress-testing affordability via the Financial Consumer Agency of Canada's mortgage calculator (canada.ca).

Practical Tips for Canadians Choosing in 2026

With renewals pressuring budgets, here's actionable advice:

- Stress Test Your Budget: Qualify at higher rates (BoC stress test at ~6%). Use CMHC tools for scenarios.

- Shop Around: Compare via Ratehub or nesto; discounts vary by LTV, credit.

- Consider Hybrids: Some lenders offer fixed-variable blends for balance.

- Renewal Prep: Contact your lender 120-180 days early; explore prepayment options without penalties.

- TFSAs/RRSPs for Down Payments: Boost equity to lower rates; CRA allows Home Buyers' Plan withdrawals.

- Lock Fixed if Risk-Averse: Ideal for Vancouver/Toronto renewals amid high shelter costs.

For variable fans, ensure a buffer—EI or CPP alone won't cover shocks.

Regional Impacts Across Canada

Housing varies: average $670k nationally, but $1M+ in BC/ON means bigger payments. Prairies see stable variables suiting commodity workers; Atlantic Canada favours fixed amid tourism volatility. StatCan data shows renewals hitting urban fixed holders hardest.

Next Steps for Your Mortgage Decision

Run numbers with a broker today—don't wait for renewals. Use canada.ca's affordability tools, consult CRA for tax perks, and track BoC updates. Whether fixed for security or variable for potential savings, align with your risk tolerance and timeline. Secure your rate before shifts hit.

Frequently Asked Questions

Sources & References

-

1

Mortgage Rates Forecast Canada 2025-2029 — www.nesto.ca

-

2

Mortgage Rate Forecast (2025-2030) — www.truenorthmortgage.ca

- 3

-

4

Canada Mortgage Rate Forecast 2025 to 2027 — www.mortgagesandbox.com

- 5

-

6

Canada Interest Rate Forecast 2026-2031 — myperch.io

-

7

Policy Interest Rate — www.bankofcanada.ca

-

8

Interest Rates Up, or Down, in 2026: Bank of Canada — www.youtube.com

-

9

2025 Housing Market Outlook — www.cmhc-schl.gc.ca