How to Invest in Canadian REITs 2026: Real Estate Without Owning Property

Imagine gaining exposure to Canada's thriving real estate market—from bustling industrial warehouses to stable residential apartments—without the hassle of property management, tenant issues, or hefty...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine gaining exposure to Canada's thriving real estate market—from bustling industrial warehouses to stable residential apartments—without the hassle of property management, tenant issues, or hefty down payments. In 2026, Canadian Real Estate Investment Trusts (REITs) make this possible, offering steady dividends, diversification, and liquidity right from your brokerage account.

With interest rates stabilising and sectors like industrial logistics and seniors housing showing strength, now's an ideal time for Canadians to explore REITs. Whether you're saving for a home down payment, building retirement income, or simply diversifying beyond stocks and bonds, this guide walks you through how to invest in Canadian REITs in 2026.

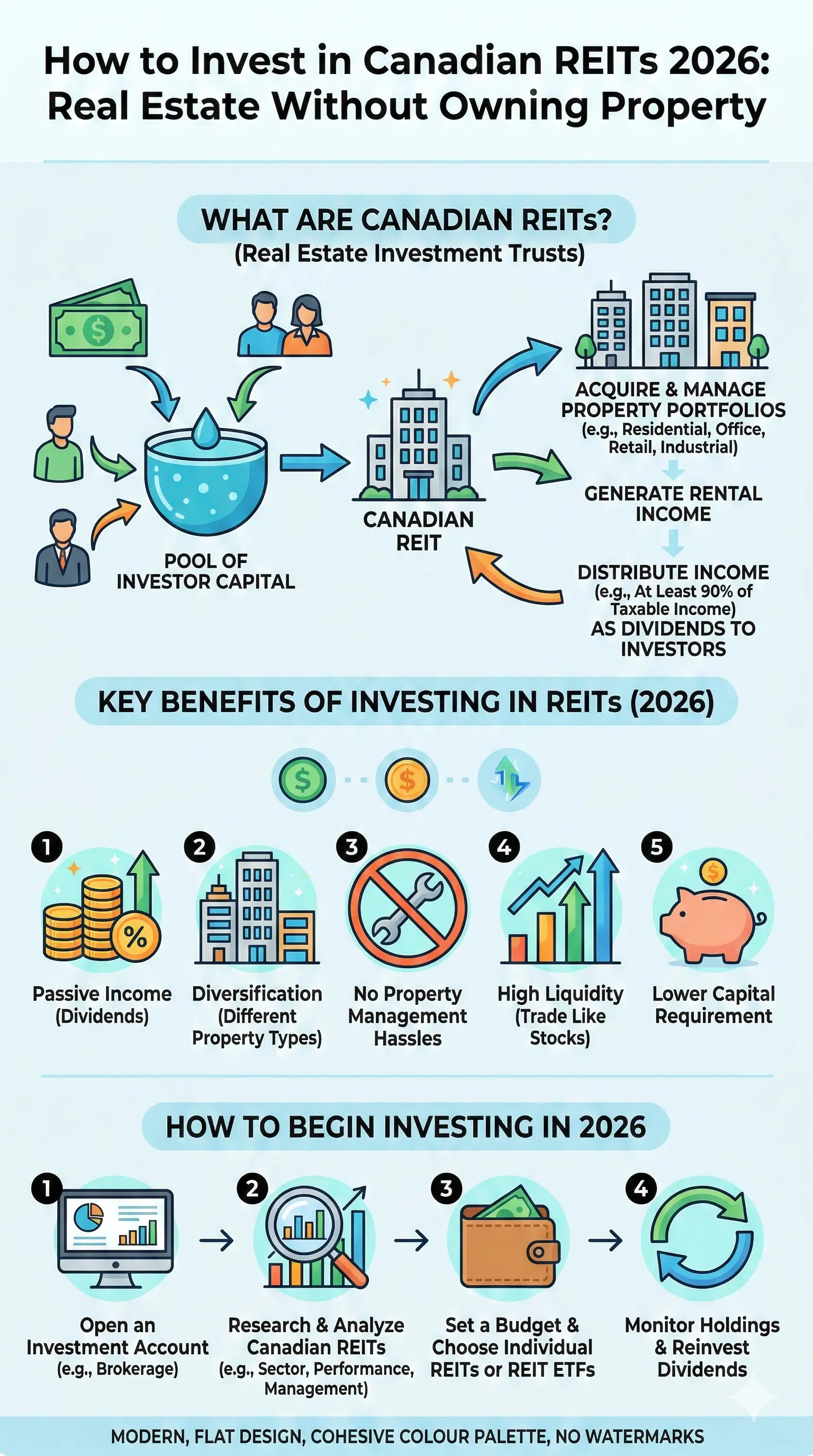

What Are Canadian REITs?

Real Estate Investment Trusts (REITs) are companies that own, operate, or finance income-generating real estate. They pool investor money to buy properties like apartments, shopping centres, offices, and warehouses, then distribute at least 90% of their taxable income as dividends. This structure delivers high yields—often higher than traditional dividend stocks—while letting you invest in real estate without owning physical property.

In Canada, most REITs trade on the Toronto Stock Exchange (TSX) as units (e.g., GRT.UN), behaving like stocks but focused on real estate cash flows. Unlike direct property buys, REITs offer liquidity—you can sell shares anytime during market hours—and professional management.

Why REITs Appeal to Canadians in 2026

- Passive Income: Yields average 4-7%, with many REITs raising payouts to match inflation.

- Diversification: Real estate moves differently from stocks or bonds, hedging against market volatility.

- No Landlord Duties: Skip repairs, evictions, and vacancies.

- Tax Efficiency: Dividends qualify for the dividend tax credit in non-registered accounts; hold in RRSPs or TFSAs for sheltering.

- Accessibility: Start with as little as $100 via fractional shares on platforms like Wealthsimple.

Financial planners often suggest allocating 5-10% of your portfolio to REITs for balance.

Types of Canadian REITs to Consider in 2026

Canada's REIT market spans diverse sectors, each with unique risks and opportunities. Industrial and residential REITs lead amid e-commerce growth and housing shortages.

Industrial REITs

These own warehouses and distribution centres, fuelling online shopping. Demand for same-day delivery keeps occupancy high with long-term leases.

- Granite REIT (GRT.UN): Industrial focus with 4.4% yield and 15-year dividend growth; 2025 YTD return +11.8%.

- Dream Industrial REIT (DIR.UN): Prime urban assets for e-commerce; top pick for long-term total returns.

Residential REITs

Amid Canada's rental boom, these manage apartments and condos. Stable as population grows and homeownership stays challenging.

- Boardwalk REIT (BEI.UN): Western Canada residential; 2.4% yield with growth potential.

- Killam Apartment REIT (KMP.UN): Atlantic Canada focus; attractive rents in underserved markets.

- CAPREIT (CAR.UN): Largest multi-residential; 3.9% yield, trading at a discount.

Retail REITs

Grocery-anchored centres prove recession-resistant. Avoid pure mall plays; opt for necessity retail.

- SmartCentres (SRU.UN): 7.2% yield; defensive with development upside.

- Choice Properties (CHP.UN): Loblaw-backed; 6.2% yield.

- CT Real Estate Investment Trust (CRT.UN): Canadian Tire anchor; reliable income.

Healthcare and Other REITs

Seniors housing thrives with Canada's aging population.

- Chartwell Retirement Residences (CSH.UN): 3.8% yield; demographic tailwinds.

Step-by-Step: How to Invest in Canadian REITs in 2026

Getting started is straightforward for Canadians. Follow these actionable steps.

Step 1: Open or Choose a Brokerage Account

Use a discount broker like Questrade, Wealthsimple Trade, TD Direct Investing, or RBC Direct Investing. They're regulated by IIROC, offer low/no commissions, and support RRSPs, TFSAs, and non-registered accounts. Wealthsimple suits beginners with fractional shares.

Tip: Fund via bank transfer or CRA direct deposit for EI/CPP to maximise tax-sheltered growth.

Step 2: Research and Select REITs

Evaluate by yield, occupancy (aim for 95%+), debt levels, dividend history, and sector outlook. Use free tools like Yahoo Finance, TMX Money, or your broker's screener. Focus on TSX-listed units for Canadian tax treatment.

Start with top 2026 picks like Granite, Boardwalk, or SmartCentres.

Step 3: Consider REIT ETFs for Diversification

If picking individuals feels overwhelming, buy ETFs. They spread risk across 10-20 REITs.

- CI First Asset REIT ETF (RCI.UN): Actively managed; top performer in residential/industrial/seniors.

ETFs trade like stocks with lower volatility than single REITs.

Step 4: Buy and Monitor

Invest what you can afford—start small. Use dollar-cost averaging: buy fixed amounts monthly to smooth volatility. Reinvest dividends via DRIP (Dividend Reinvestment Plan) for compounding.

Review quarterly: Check earnings, occupancy, and rate changes via SEDAR+ filings.

Step 5: Understand Taxes

REIT distributions mix return of capital (tax-deferred), capital gains, and income. Track via T3 slips. Hold in TFSA/RRSP to avoid immediate tax; use non-registered for dividend credit. Consult CRA guidelines or a tax advisor.

Pros and Cons of Investing in Canadian REITs

| Pros | Cons |

|---|---|

| High yields (4-7%) | Interest rate sensitivity—rising rates can pressure prices |

| Liquidity and low entry barrier | Sector risks (e.g., office vacancies post-COVID) |

| Inflation hedge via rent hikes | Dividend cuts possible in downturns |

| Professional management | Less control than direct property |

Limit to 5-10% of portfolio to manage risks.

2026 Outlook for Canadian REITs

Rate stability boosts refinancing, while industrial/residential demand persists. Watch Alberta's resource cycles and Montreal's growth. Capital markets rose 25% in 2024, signalling confidence.

FAQ

Are Canadian REITs a good investment in 2026?

Yes, for income and diversification, especially industrial and residential amid housing shortages. Yields beat GICs, but diversify.

What's the minimum to start investing in REITs?

As little as $10-100 with fractional shares on Wealthsimple or Questrade.

Do REIT dividends count as eligible dividends?

No, they're mostly return of capital or other income. Best in registered accounts.

Can I invest in REITs in my TFSA or RRSP?

Absolutely—ideal for tax-free growth on distributions.

How do REITs perform vs. direct real estate?

REITs offer liquidity and lower costs but less leverage/upside than owning property.

Are there REIT ETFs for beginners?

Yes, like RCI.UN for instant diversification.

Ready to tap into real estate income? Open a brokerage account today, research top picks like Granite or Dream Industrial, and start with a modest position or ETF. Monitor via your platform's tools, reinvest dividends, and consult a financial advisor for personalised fit. Canadian REITs in 2026 deliver property-like returns without the property headaches—build your portfolio now.