RRSP Contribution Deadline 2026: How to Reduce Your Tax Bill

With just days left until the clock runs out, many Canadians are scrambling to slash their 2025 tax bill. If you're earning a solid income this year, a timely RRSP contribution could unlock a hefty re...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

With just days left until the clock runs out, many Canadians are scrambling to slash their 2025 tax bill. If you're earning a solid income this year, a timely RRSP contribution could unlock a hefty refund from the CRA—potentially thousands of dollars back in your pocket before you know it.

Today, February 25, 2026, marks the final stretch before the RRSP contribution deadline 2026 on March 2. Don't let this opportunity slip away. In this guide, we'll break down everything you need to know about maximising your RRSP for 2025, from deadlines and limits to smart strategies that fit Canadian tax rules. Whether you're a first-time contributor or a seasoned saver, these steps will help you reduce your tax bill effectively.

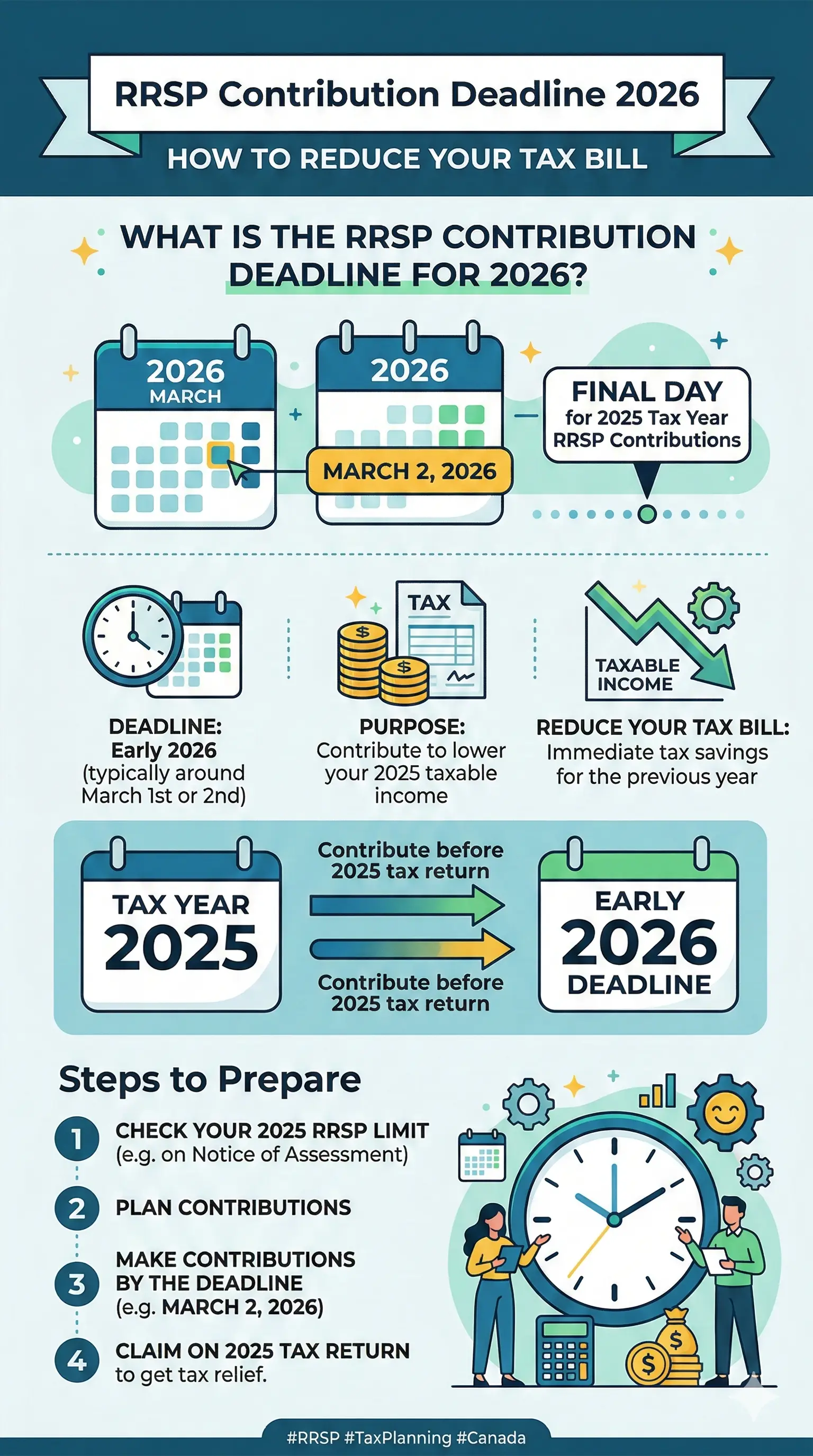

What is the RRSP Contribution Deadline for 2026?

The key date for RRSP contribution deadline 2026 is March 2, 2026—this is your last chance to contribute for the 2025 tax year. Contributions made by this deadline (the first 60 days of 2026) can be deducted from your 2025 taxable income, lowering what you owe or boosting your refund.

Contributions after March 2 generally count toward your 2026 tax year, unless you choose to carry them forward. For context, past deadlines include March 3, 2025, for 2024. Mark your calendar: financial institutions must receive your funds by end of day March 2 to qualify.

Why Act Now? The Tax Savings Power of RRSPs

RRSPs let your investments grow tax-deferred until withdrawal, meaning no annual taxes on gains, dividends, or interest. A contribution directly reduces your taxable income. For example, if you're in Ontario's 29.65% marginal tax bracket (on income $51,446–$102,894) and contribute $5,000, you could save around $1,482 in taxes.

This refund can then be reinvested, kickstarting compound growth. Early contributions (ideally January) give your money a full extra year to grow compared to waiting until deadline.

Your 2025 RRSP Contribution Limit Explained

The Government of Canada sets your annual RRSP room at 18% of your previous year's earned income, up to a maximum of $32,490 for 2025. For 2026 contributions, this rises to $33,810.

Unused room carries forward indefinitely, so check your total available space. Log into CRA My Account or review your latest Notice of Assessment to find your exact limit—it's listed in the RRSP/TFSA section.

Overcontribution Risks

Exceed your limit by more than $2,000, and you'll face a 1% per month penalty tax on the excess until corrected. Always verify your room first to avoid this costly mistake.

Step-by-Step: How to Make RRSP Contributions Before March 2, 2026

- Check Your Limit: Visit CRA My Account online or call 1-800-959-8281.

- Choose Your RRSP: Use an existing one or open a new self-directed RRSP at your bank, credit union, or investment firm.

- Fund It: Transfer via online banking, wire, or cheque. Set up pre-authorized contributions (PACs) for automatic monthly deposits to build habits.

- Confirm Receipt: Get a contribution receipt by late March for your tax return. File by April 30, 2026, to claim the deduction.

- Claim the Deduction: Enter it on Schedule 7 of your T1 return; refunds arrive 2–8 weeks later.

For last-minute moves, many banks offer same-day processing if initiated early.

Smart RRSP Strategies to Maximise Tax Savings in 2026

1. Calculate Your Optimal Contribution

Use free CRA-approved calculators to estimate savings. A $10,000 contribution in B.C.'s top 20.5% provincial bracket (plus federal) could yield over $4,000 back. Prioritise if you're in a high bracket now but expect lower income in retirement.

2. Spousal RRSPs for Income Splitting

Contribute to a lower-income spouse's RRSP to split future retirement income, reducing overall taxes. Attribution rules apply if withdrawn within three years.

3. Carry Forward Unused Room

Got room from prior years? Pile it on now for bigger deductions. No time limit on carry-forwards.

4. Invest for Growth

Opt for low-fee ETFs or index funds inside your RRSP. With tax-deferred growth, even modest 5–7% annual returns compound powerfully over decades.

Practical Tip: The Refund Reinvestment Loop

Deposit your tax refund straight back into your RRSP or TFSA. This "loop" amplifies savings without touching your cash flow.

Common Pitfalls to Avoid Before the Deadline

- Forgetting Employer Matches: Max out group RRSPs if your workplace offers matching—free money!

- Age Limits: Contribute until December 31 of the year you turn 71.

- Withdrawal Traps: Early pulls trigger withholding tax and lost contribution room forever.

- Overlooking HBP/LLP: If repaying Home Buyers' Plan, align with deadlines like October 1 post-withdrawal.

Next Steps: Secure Your Tax Savings Today

Log into CRA My Account now, crunch your numbers with an RRSP calculator, and transfer funds before March 2. Consult a financial advisor or tax pro for personalised advice—this isn't one-size-fits-all, especially with provincial variations. Small actions today build your retirement fortress tomorrow. Start contributing, claim that refund, and watch your wealth grow.

Disclaimer: This is general information, not personalised tax advice. Tax laws change; consult a qualified professional or the CRA for your situation.

Frequently Asked Questions

Sources & References

-

1

Important dates for RRSPs, HBP, LLP, FHSAs and more — canada.ca — www.canada.ca

-

2

Last-Minute RRSP Planning: Deadline, Limits and More — rbcroyalbank.com — www.rbcroyalbank.com

-

3

RRSP Contribution Deadlines — td.com — www.td.com

-

4

2025 RRSP Tax Savings Calculator — turbotax.intuit.ca — turbotax.intuit.ca

-

5

Important Tax Dates in Canada 2025: Deadlines — hrblock.ca — www.hrblock.ca

-

6

Three Key Considerations for RRSP Season ETFs — harvestportfolios.com — harvestportfolios.com

-

7

RRSP contribution deadline — nbc.ca — www.nbc.ca