Income Splitting Canada 2026: Legal Ways to Reduce Your Family Tax Bill

Imagine slashing your family's 2026 tax bill by thousands of dollars—all legally and without breaking a sweat. That's the power of income splitting in Canada, a smart strategy that shifts income from...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine slashing your family's 2026 tax bill by thousands of dollars—all legally and without breaking a sweat. That's the power of income splitting in Canada, a smart strategy that shifts income from higher earners to lower ones, leveraging our progressive tax system to your advantage. With Tax on Split Income (TOSI) rules evolving and new opportunities emerging, Canadian families can still optimise their taxes in 2026. Let's dive into the legal ways to make it happen.

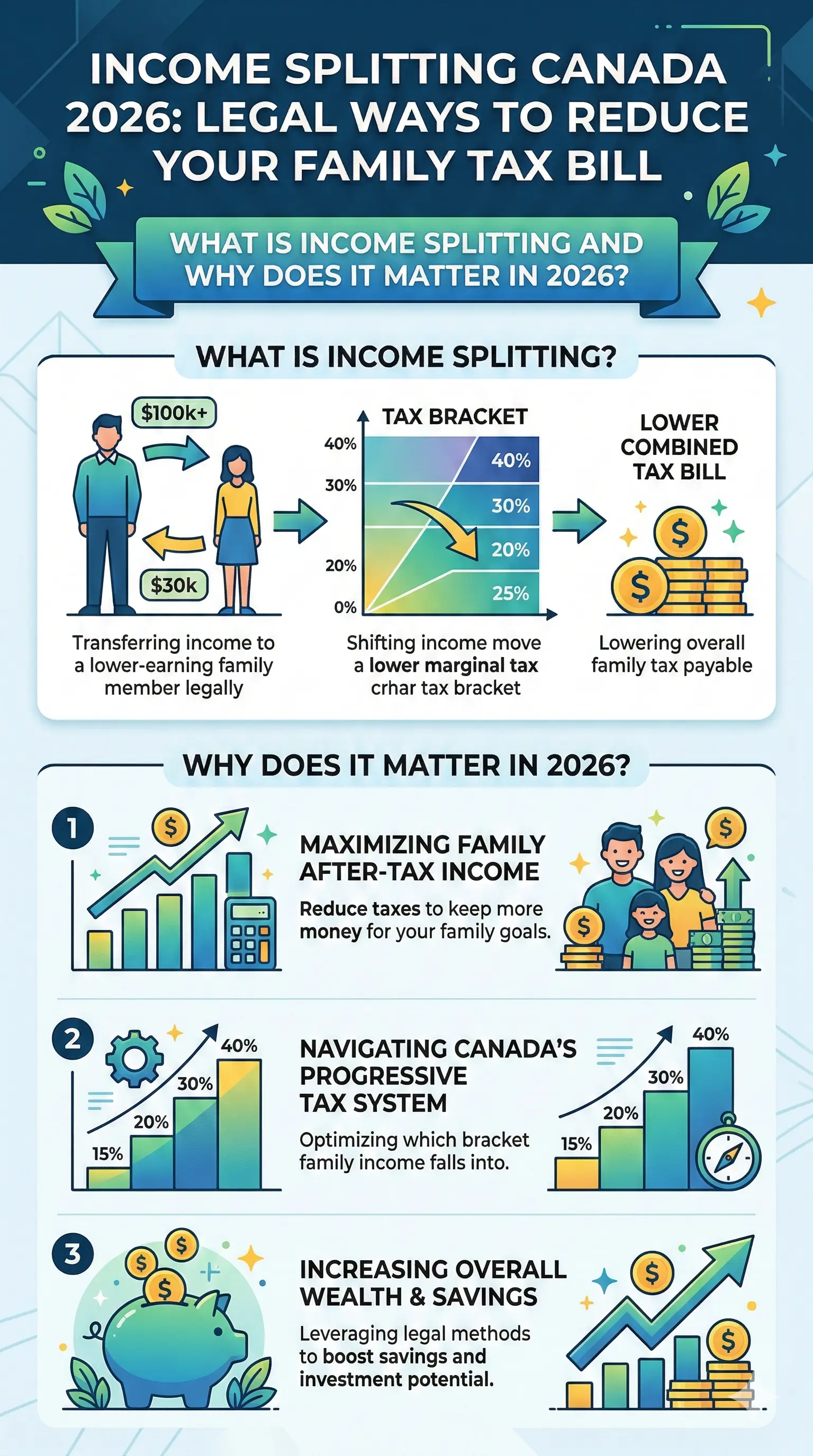

What is Income Splitting and Why Does it Matter in 2026?

Income splitting involves allocating income to family members in lower tax brackets, reducing your household's overall tax burden. Canada's graduated tax system means higher earners face steeper rates—for instance, in 2026, federal tax is 14% on income up to $58,523 but jumps to 20.5% on amounts up to $117,045. Two spouses earning $100,000 each pay less tax than one earning $150,000 and the other $50,000, making splitting a game-changer.

In 2026, TOSI rules continue to limit aggressive splitting, taxing certain split income at the top marginal rate for recipients over 18 (previously just under 18). Exceptions exist, like for 18-24-year-olds working 20+ hours weekly. Despite these hurdles, legal methods abound for families, couples, and retirees.

The Impact of TOSI on Your Strategy

TOSI targets "split income" such as dividends from family businesses, taxing it at the highest rate unless exceptions apply—like meaningful labour contribution or reasonable business returns. Use Form T1206 to calculate this tax, and claim a deduction on line 23200. Plan around it: focus on CRA-approved tactics below.

Legal Income Splitting Strategies for Canadian Families in 2026

Here are proven, CRA-compliant ways to split income. Tailor them to your situation—spouses, common-law partners, or adult kids—and consult a tax pro for personalised advice.

1. Spousal or Common-Law RRSP Contributions

The higher earner contributes to a spousal RRSP, using their deduction room at their higher marginal rate. Withdrawals later are taxed in the lower earner's hands. No age limit for the contributor; it's flexible year-to-year. Example: If you're in the 40% bracket and your spouse is in 20%, a $10,000 contribution saves $2,000 upfront, with future withdrawals taxed lightly.

- Action step: Check contribution room via CRA My Account.

- Tip: Time withdrawals to avoid attribution rules.

2. Pension Income Splitting

Canadians 65+ (or any age for certain survivor pensions) can split up to 50% of eligible pension income with a spouse or common-law partner. Eligible income includes RRIF/RRSP annuities, life annuities, and CPP/QPP benefits (but not post-retirement CPP). Both must live together in Canada, with exceptions for temporary separations.

File Form T1032 jointly by your tax deadline—it's electable annually, so adjust percentages yearly. Younger than 65? Split qualifying life annuities or death-related payments.

| Income Type | Eligible for Splitting? | Notes |

|---|---|---|

| RRIF minimums (line 11500) | Yes | Up to 50% |

| CPP/QPP retirement pension | Yes | Based on cohabitation months |

| OAS or foreign IRA | No | Not eligible |

3. Prescribed-Rate Loans

Lend money to your lower-income spouse or adult family member at the CRA's prescribed rate (currently low in 2026). They invest it, and net income (after interest) is taxed in their hands. No TOSI if structured right—pay interest annually by January 30.

Example: Loan $100,000 at 2% ($2,000 interest). Spouse earns 5% ($5,000); nets $3,000 taxed at their low rate. You deduct interest paid.

4. TFSA and Other Registered Accounts

While not direct splitting, max your combined TFSA room—$109,000 cumulative by 2026 for those eligible since 2009. Lower earner withdraws tax-free. Gift funds to spouse's TFSA (no attribution rules apply).

5. CPP/QPP Sharing and Other Tactics

Share CPP/QPP based on cohabitation during contributions. For businesses, pay reasonable salaries to working family (avoiding TOSI). Consider family trusts or estate freezes cautiously, as TOSI applies broadly.

Step-by-Step: Implementing Income Splitting for 2026 Taxes

- Assess brackets: Use CRA's 2026 tax tables to compare marginal rates.

- Gather docs: T1032 for pensions, loan agreements for prescribed loans.

- File jointly: Ensure matching info on returns.

- Track changes: Amend via new T1032 or revocation letter if needed.

- Monitor TOSI: Complete T1206 for at-risk income.

Pro tip: Use tax software or a CPA to simulate scenarios—savings can hit 20-30% on shifted income.

Common Pitfalls and How to Avoid Them

- TOSI traps: Don't split business dividends without labour contribution.

- Residency rules: Both must reside in Canada.

- Age myths: Pension splitting isn't 65+ only for all types.

- Foreign income: No splitting for OAS or IRAs.

FAQ: Income Splitting Canada 2026

Is income splitting legal in Canada?

Yes, fully legal when following CRA rules, though TOSI may apply to certain splits.

Do both spouses need to be 65 for pension splitting?

No—the receiving spouse can be younger; eligible income includes annuities for all ages in some cases.

What's the TOSI exemption for young adults?

18-24-year-olds working 20+ hours/week on average are exempt.

Can I split income with kids over 18?

Limited by TOSI, but prescribed loans or salaries for contributors work.

How much pension income can I split?

Up to 50%, elected yearly via T1032.

Does Quebec differ?

Yes, rates vary (e.g., 19-29% on splits over $5,000).

Next Steps to Cut Your 2026 Family Tax Bill

Start by reviewing your 2025 return for 2026 planning. Max spousal RRSPs before March 1 for 2025 deductions, set up prescribed loans now, and elect pension splits when filing. Tools like CRA My Account or free tax estimators help. For complex setups, book a CPA—savings often exceed fees. Remember, tax laws evolve; this isn't advice—seek professional guidance tailored to your family.