How to Get a Mortgage With Bad Credit in Canada 2026

Struggling with a low credit score but dreaming of homeownership in Canada? You're not alone—many Canadians face this challenge, yet it's still possible to secure a mortgage in 2026 with the right str...

The Lifetimes Canada editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes Canada readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Struggling with a low credit score but dreaming of homeownership in Canada? You're not alone—many Canadians face this challenge, yet it's still possible to secure a mortgage in 2026 with the right strategy and lenders.

Whether past financial setbacks like missed payments or high debt have dinged your score, options exist beyond the big banks. This guide breaks down how to get a mortgage with bad credit in Canada 2026, from improving your score to tapping alternative lenders and government programs. We'll cover practical steps tailored for our market, including CMHC rules and down payment tips, so you can take action today.

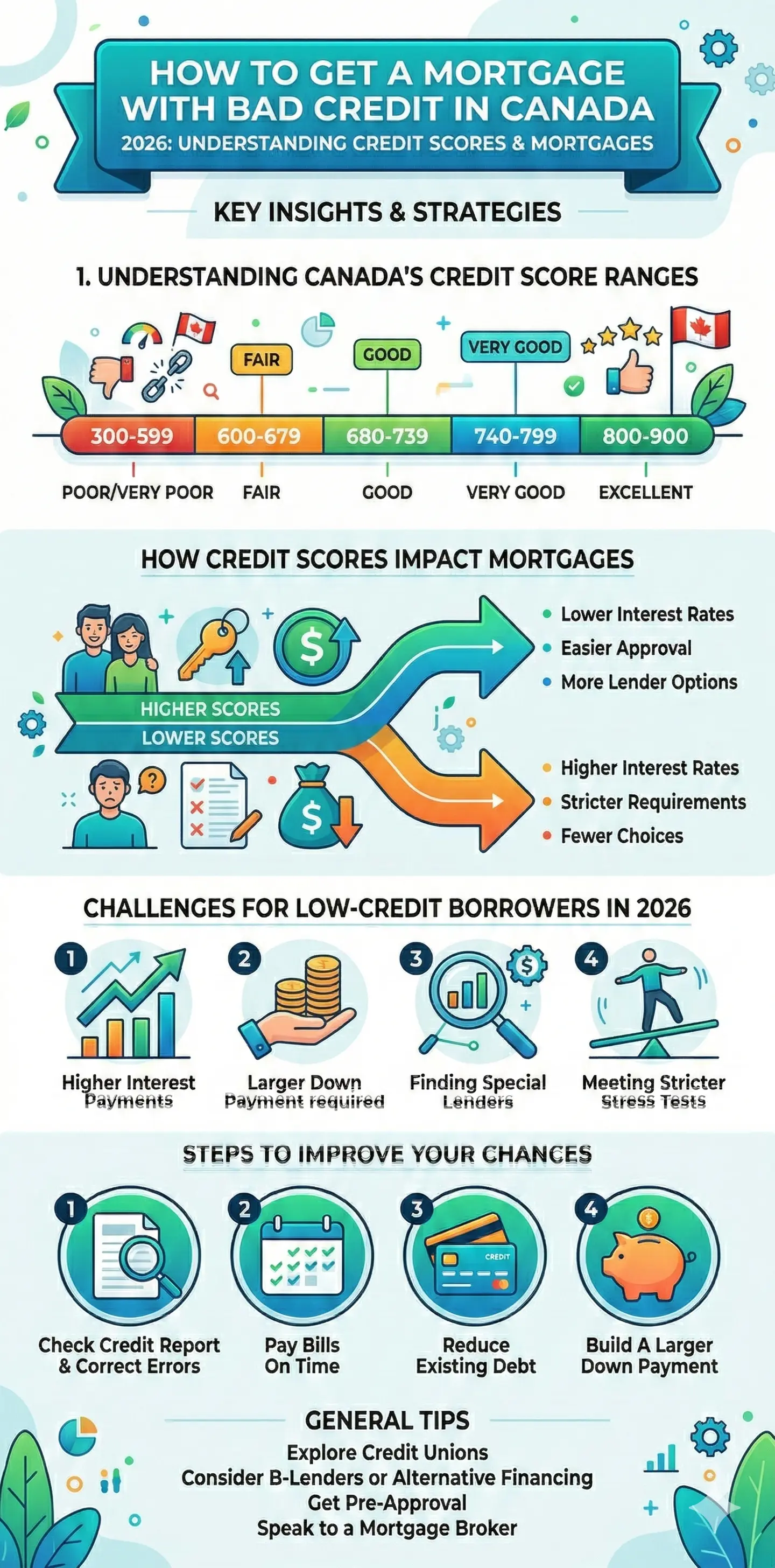

Understanding Credit Scores and Mortgages in Canada

Canadian credit scores range from 300 to 900, managed by Equifax and TransUnion. Scores below 650 are often seen as problematic for conventional mortgages, while big banks typically want 680 or higher for approval.

What Counts as Bad Credit?

- Below 600: Most major banks won't approve you, pushing you toward B lenders or private options.

- 600-680: Possible with CMHC-insured mortgages or credit unions, but expect scrutiny.

- Below 560: Considered poor, making even alternative lending tougher without a strong down payment.

Lenders assess more than just your score—they review income stability, debt ratios, and assets. For instance, Gross Debt Service (GDS) ratios can't exceed 39% for CMHC-insured loans.

Steps to Get a Mortgage with Bad Credit

Follow these actionable steps to boost your chances in 2026's market, where interest rates and insurance rules continue to evolve.

Step 1: Check and Improve Your Credit Score

Pull your free credit reports from Equifax and TransUnion to spot errors. Focus on payment history (35% of your score), credit utilization (under 35%), and avoiding new applications.

- Pay bills on time—set up pre-authorized debits.

- Reduce debt: Aim to pay down credit cards before applying.

- Keep old accounts open to build history, especially if you're a newcomer with thin credit.

Improving from bad to fair (600+) can take 6-12 months but opens doors to better rates.

Step 2: Save a Larger Down Payment

The minimum down payment is 5% on the first $500,000 of your home's price (plus 10% on the rest), but with bad credit, target 20-25% to avoid CMHC insurance and show commitment.

For a $500,000 home, a 20% down payment ($100,000) skips insurance premiums, lowering your monthly costs. Use the Home Buyers’ Plan (HBP) to withdraw up to $60,000 tax-free from your RRSP for this—repay over 15 years.

| Down Payment | Amount for $500k Home | CMHC Insurance Needed? | Monthly Savings Example (2.54% rate, 25-yr amort.) |

|---|---|---|---|

| 5% | $25,000 | Yes | - |

| 20% | $100,000 | No | ~15-20% lower payments |

Step 3: Explore Alternative Lenders

When banks say no, turn to these Canada-specific options:

- B Lenders: Trust companies and finance firms for scores 500+. Higher rates (1-3% above prime), but flexible on job stability or recent bankruptcies.

- Credit Unions: Provincially regulated, some skip the mortgage stress test. Check Innovation Federal Credit Union's Fresh Start Mortgage for bruised credit.

- Private Lenders: Last resort for recent consumer proposals; short terms (1-3 years), high rates (8-12%), but can bridge to better credit.

Mortgage brokers connect you to these without bias—many work nationwide.

Step 4: Leverage Government Programs

CMHC insurance covers down payments under 20%, requiring a minimum score of 600 (one borrower). Not available for homes over $1.5 million. Pair with HBP for stronger applications.

First-Time Home Buyer Incentive (if available in 2026) shares equity to reduce payments—check canada.ca for updates.

Pros and Cons of Bad Credit Mortgages

| Pros | Cons |

|---|---|

| Access homeownership despite low scores | Higher interest rates (up to 3% more) |

| Flexible criteria via B lenders | Larger down payments required |

| Build equity and improve score over time | Shorter terms, frequent renewals |

Common Pitfalls to Avoid

- Skipping the stress test: Even alternatives may qualify you at higher rates.

- Overlooking property type: Lenders scrutinize condos (25% down often needed).

- Ignoring total costs: Factor in closing fees (1.5-4% of price) and land transfer tax.

"A larger down payment signals financial stability and can offset credit concerns."

FAQ

Can I get a mortgage in Canada with bad credit?

Yes, via B lenders, credit unions, or private options if your score is 500+. Expect higher rates and 20%+ down.

What's the lowest credit score for a mortgage?

Big banks need 600-680; alternatives start at 500. CMHC requires 600 for insured loans.

Do I need mortgage insurance with bad credit?

Only if down payment <20%. A 20%+ down avoids it entirely.

How long after bankruptcy can I get a mortgage?

Typically 2+ years for B lenders; private sooner but costlier.

Are credit unions better for bad credit?

Often yes—more flexible, no federal stress test in some provinces.

Can newcomers get bad credit mortgages?

Thin credit history hurts, but document income and save 20%+ to qualify.

Next Steps to Homeownership

Start by checking your credit today, then consult a mortgage broker via the Financial Services Regulatory Authority of Ontario (FSRA) or your province's equivalent. Save aggressively, explore HBP, and target B lenders. With discipline, you'll not only get approved but build long-term wealth. Contact a broker now—many offer free pre-approvals tailored for 2026 rates.